ACT Research offered more insight into the state of Class 8 truck orders and trailer orders in two recently released reports.

The company wrote in its State of the Industry: North American Classes 5-8 report that it has yet to determine if January's soft heavy-duty truck order totals were a single-month blip or the beginning of a more broad-based pullback in demand. The company says medium- and heavy-duty seasonal orders remained robust, so it will take more time to determine what January's total represents.

Eric Crawford, ACT Research's vice president and senior analyst says heavy-duty retail sales were up 29% year over year on a seasonally adjusted basis. Additionaly, the market's 1,389 units per day rate was nearly 23% ahead of the year-ago rate, 15.5% above the full-year 2022 average, and up 4.5% month over month.

“Business activity in the truck industry rolls on, with retail sales seemingly unphased by higher interest rates, as pent-up demand remains, for now. We expect this dynamic to shift in the second half of 2023, as the Fed continues its aggressive push to subdue inflation,” he says.

[RELATED: Retail used truck volumes recovering?]

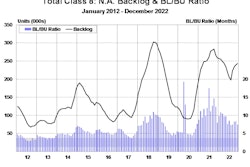

In the trailer space the company's analysis showed the backlog-to-build ratio increased to 9.9 months after averaging 8 months since August of 2021 but actually trended down on a seasonally adjusted basis. Despite the later downturn, ACT Research says the current totals indicate the trailer industry is “essentially committed” into the beginning of the fourth quarter of 2023.