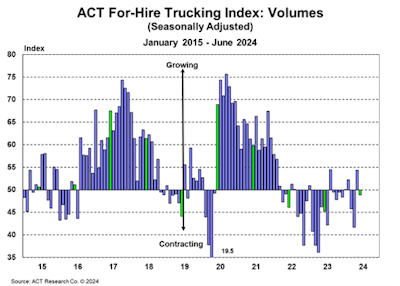

The latest release of ACT’s For-Hire Trucking Index suggests the supply-demand balance between the fleet and freight is narrowing, ACT Research reported Thursday.

ACT states the Volume Index decreased 5.5 points in June to 48.9, seasonally adjusted (SA), from a Roadcheck-assisted 54.4 in May.

“Volumes have been fairly flat this year, but they’ve improved to ‘less worse’ on a year over year basis, with the index averaging 48.8 through the first half of this year, versus 42.8 last year,” says Carter Vieth, research analyst at ACT Research. “Even with consumers under strain, real U.S. retail sales are up 1.8% year to date, and further disinflation helps support our outlook on real income growth.

“Additionally, intermodal and import volumes are trending positive, which minimally adds to overall surface freight volumes. Private fleet insourcing has likely taken away some for-hire demand, but the recent softening in U.S. Class 8 tractor sales indicates a slowing in private fleet growth.”

[RELATED: Investigating Beryl's impact on seasonal freight patterns]

Additionally, the company states truckload volume data remain mixed, with the Cass Freight Index and DAT spot loads still at cycle lows. The Capacity Index also increased by 3.6 points month over month to 49.3 in June, from 45.6 in May.

“Though the index increased month over month, this month’s For-Hire Supply Demand Balance June 2024 reading marks the 12th month in a row capacity has been below 50, the longest streak of decline since the inception of the survey in late 2009,” Vieth says. “Fleet capacity contractions occurring at a slower rate suggest the supply-demand balance between the fleet and freight is narrowing. Given the duration of this downturn and the still-weak fundamentals, it’s hard to see capacity turning positive in the coming months, especially as the US tractor sales trend continues to sag.”

Finally, the Supply-Demand Balance fell in June to 49.6 (SA), from 58.7 in May, as freight volumes decreased and fleet capacity increased.

“Private fleet expansion, which is not captured in this indicator, is resulting in a longer leadup to higher market rates than in past cycles. With capacity an issue, overall equipment purchasing trends will remain key to watch. Continuing demand-side freight growth should provide ongoing support to the market balance,” Vieth adds.