Affordable Care Act premiums made headlines at the end of 2025 with premiums increasing by almost 30% in some cases. But for most Americans, health insurance comes via their employer and an employer-sponsored health insurance plan (ESI). It’s part of an employee’s compensation package along with pay, time off and other common benefits.

Businesses that offer ESIs are seeing premium increases too, though not as drastic. For businesses with a tight margin, those increases can be crippling, affecting hiring decisions, capital expenditures and more.

How many people are covered by employer insurance?

ESIs cover about 150 million people in America under the age of 65, non-profit health policy research, polling and news organization KFF says, costing employers about $19,276 per covered family, on average, with employees sharing an additional $6,296 of the cost. For employee-only coverage, premiums average $9,325 with an increase of 5%. Nationally, the organization says 59% of small firms and 97% of large firms offer health benefits to at least some workers.

One of those small firms is First Call Truck Parts, which has three locations in south Georgia and north Florida.

“We didn’t have (insurance) for 20 years,” says Jon Ward, First Call’s CFO. The company, which has around 20 employees, now offers what Ward calls “the Honda Civic” of insurance plans. It’ll get you to care, but it’s not anything fancy.

“It’s not ideal,” he says. “Nothing with health insurance is.”

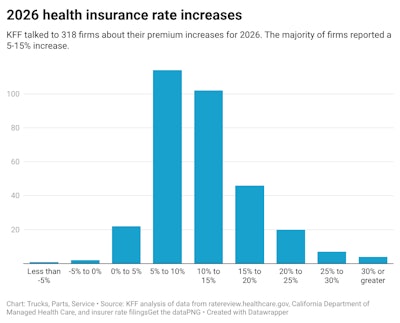

How much have premiums increased for businesses?

The size, location and industry can affect how much premiums have gone up — and almost universally, they’ve gone up. KFF says businesses saw an 11% median premium increase. Across 16 states and the District of Columbia, KFF found insurers proposed a median rate increase of 12%. Only three insurers asked for a decrease, it says.

In the 2025 annual survey, KFF found the average family premium increased 26% since 2020 and 53% since 2015. Increases depended on where the companies were located, the industry they were in, and the number of employees.

Smaller businesses tend to have a tougher time handing these increases, says the National Federation of Independent Business. It’s a non-profit, non-partisan organization representing small and independent business owners. Health insurance affordability is a crisis for small business, it says.

“For nearly 40 years, NFIB members have consistently identified the rising cost of health insurance as their No. 1 business concern,” NFIB says in a report. “The small group market, where most small businesses purchase coverage, is in a death spiral.”

It cites the contraction of insurance company participation in the market, sending rates soaring. KFF says fewer companies are also offering the benefit; last year, 61% of firms with 10 or more workers offered health benefits, lower than the 68% reported five years ago. The likelihood of offering insurance increases with the number of workers a business has. More than 90% of firms with 50 or more workers offered health benefits in 2025, KFF says.

Why are premiums so high?

Businesses report several reasons for increases in premiums. The majority (71%) of large firms (more than 200 workers) say prescription drug prices contributed at least somewhat to higher premiums. Nearly that many (69%) also say the prevalence of chronic diseases play at least some of a role, followed by a higher utilization of health care services, higher prices for hospital services and new prescription drugs.

NFIB surveys small businesses every so often on their biggest problems and priorities. Its latest Small Business & Priorities was released in 2024. In that survey, 41% of small business cited the cost of health insurance as critical, keeping the No. 1 position in the survey that it’s held since 1986.

“Health insurance has been a continuous challenge for small business owners,” says Holly Wade, executive director of NFIB’s Research Center. “The cost of health insurance is by far the biggest challenge for employers who offer health insurance and for those who do not offer it. Small employers compete for talent in filling open positions and are aware that health insurance is an important benefit for many employees and job seekers.”

Plans attract employees

Ward says First Call started offering a plan because it was missing out on employment opportunities. With just 20 employees, he’s not subject to penalties imposed by the ACA, but chose to offer coverage as a benefit to attract and retain talent.

“It helped some of our guys out,” he says.

Other businesses agree, even in Canada, which has universal health care. Robyn Spitzke is president of truck parts supplier Fort Garry Industries in Winnipeg, Manitoba.

“Not everything is covered by universal health care,” she says. Fort Garry offers dental care, eye care, drug coverage and more. Employees, she says, look at the entire benefits package when choosing where to work, and it’s important to have a good one to attract the best talent.

“If you want to stay in business, your cost of business continues to rise,” she says. Fort Garry looks for sales opportunities and any way it can to increase margins. It has also played around with drug coverage plans and sharing costs with employees to help mitigate some of the increases.

A complicating factor stateside, however, is that smaller firms like First Call may have less flexibility in negotiation than larger companies, which may lead to a larger part of their profits going to pay health insurance premiums. A 2024 JPMorgan Chase survey found firms with less than $600,000 in annual revenues, 12% of those were eaten by health insurance premiums. For firms with revenues greater than $2.4 million, that dropped to 7%. Furthermore, firms with fewer employees paid the highest premiums.

How to keep costs down

Unfortunately, there’s no silver bullet for keeping costs down for every business. But there are some things that are evolving in response to the spike in premiums.

The first is perhaps the most obvious but not without risk: Raising the employee share of the cost. This can be done by simply raising the portion of the premium the employee pays before taxes or by raising the deductible the employee pays when they use medical services. KFF says there has been a 23% worker contribution increase for family coverage from 2020-2025. During that same period, there was a 26% total premium increase. On average, workers contributed 16% of the premium for single coverage and 26% of the premium for family coverage.

Most workers — 88% according to KFF — have a general annual deductible that must be met before services are covered by the plan. The average deductible in 2025 for workers with single coverage was $1,886, an increase of 17% over the last five years and 43% over the last 10 years. More employers are opting for higher deductible plans, KFF says, with deductibles greater than $2,000. KFF says the number of these high-deductible plans has increased 32% over the last five years and 77% in the last 10 years.

But these choices also run the risk of doing the opposite of what health care plans are supposed to do, attract talent, and that’s a big worry. KFF says half of companies say their employees are already concerned about cost-sharing levels.

Another option that’s growing in popularity is an individual coverage health reimbursement arrangement (ICHRA) that helps employees purchase coverage in the individual market. KFF says around 8% of employers offering health benefits that are not ICHRAs are very likely or somewhat likely to offer this benefit in the next two years. Even more small firms, 18%, that don’t offer any benefits now are looking at this option as a solution.

Smaller businesses also could benefit from pooling arrangements or association health plans (AHPs), which enable businesses to band together and leverage purchasing power like a larger firm. One such rule change in 2018 made it easier for groups to form associations, including self-employed people, and specified these groups would be regulated the same as large-group coverage.

Self-funded plans are an option too, particularly for larger firms. These companies pay for health services of enrollees directly through their own funds. There also are level-funded plans, which are nominally self-funded and may be more attractive for small- and medium-sized businesses. In these arrangements, the insurer calculates an expected monthly expense, including a share of benefits, premiums for stop-loss protection and administrative fees. Stop-loss protection is a separate insurance product that protects businesses from unexpectedly expensive claims.

Business organizations push for policy relief

Organizations like the NFIB advocate for policy changes to support small businesses struggling with health care costs, such as targeted tax credits; expanded access to ICHRAs, health savings accounts (HSAs), AHPs and stop-loss coverage for level-funded plans; promoting health care price transparency and discouraging hospital consolidation to maintain competition to control prices.

“For nearly four decades, health insurance costs have been the No. 1 concern for small business owners, and we are now at a breaking point,” says Josselin Castillo, NFIB principal of federal government relations. “The small-group market is collapsing, premiums are unsustainable, and small businesses are being forced to make difficult choices. Without immediate and targeted policy reforms, millions of Americans may lose access to employer-sponsored health coverage."