Findings from the most recent Heavy Duty Manufacturers Association (HDMA) Pulse survey indicate rising economic uncertainty is changing supplier planning, yet there remains no consensus on the potential impact on the commercial vehicle supplier market.

Fleet order levels have dropped, but whether it is ongoing labor and supply chain disruptions creating availability issues, inflation hurting fleets or overall economic conditions driving the change is unknown, according to HDMA’s Richard Anderson, senior director of research and analytics.

“Even during a recession, HDMA member respondents continue to report supply chain and labor problems more commonly associated with periods of expansion,” Anderson said during Wednesday’s HDMA Pulse webinar. The Pulse poll surveys members which are made up of the commercial vehicle supply market.

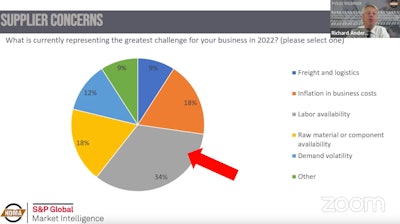

Suppliers were asked what is currently representing the greatest challenge for their business in 2022.

Topping the list at 35 percent is labor availability. Tied for second at 18 percent is inflation in business costs and raw material or component availability. Rounding out the list of concerns are demand volatility at 12 percent and freight and logistics (9 percent) and Other (9 percent).

“When we asked what their greatest challenge is today, the No. 1 answer remains labor availability; but labor availability is not typically a problem we associate during periods of recession. If we look at all of these: inflation in business costs and raw material and component availability also are not problems we associate with a recession,” Anderson said.

“What we see is some of the reasons for the confusion and why our members are having such difficulty with their planning activities and trying to understand how the rest of this year and the rest of 2023 might play out,” he said. “We’re truly operating in times when the economy is not working as the normal models would predict.”

When suppliers were asked which set of economic factors do they believe will drive fleet buying behaviors in 2023, comments included:

- Absolute need for parts.

- Consumer confidence, retail sales and housing.

- Continued pressure to reduce carbon emissions in 2024 will push fleets to purchase in 2023.

- Fleet profitability drives their buying behaviors.

- Freight demand will be a bigger factor in 2023. We’ve met the technical definition of recession these last two quarters and if it continues or deepens, the freight demand becomes the bigger question.

- Infrastructure spending converting to actual work in progress. Also, an uptick in housing construction, especially single-family at the “entry/affordable” end of the scale.

- Pent up demand to replace an aging fleet.

Turning to demand of Class 4-8 trucks in North America, Andrej Divis, executive director, Global Heavy Truck Research, S&P Global, says the industry is at around a half million units annualized rate in the U.S. and it’s very mixed by weight class.

“We had a very strong recovery this year in Class 8, really shooting up strongly, led by tractor trucks. Vocational trucks not so much, but tractor trucks have been bringing the market up. Of course, Class 8 is about half the market. When we look at the other half of the market, we look at mediums and what we’ve seen there is the heavy side, Class 6-7, they’ve been rebounding strongly as well, while we see Class 4-5 start to weaken and decline,” Divis said.

There are varied reasons behind these trends.

“Some of them have to do with supply chain and availability. Our data shows the situation with production capacity is improving better with Class 8 than the medium-duty overall and one of the pieces of evidence for that is that the inventories are coming back. We’re getting a better balance between vehicles going to owners but also having inventory pushing through the system,” he said.

When addressing the forecast for truck demand, Divis stressed S&P Global is not assuming a significant global recession in the baseline forecast. It does believe, however, there will be some areas of significant slowdown or even slight contraction.

“We’re expecting 2022 on a Class 4-8 basis to be flat or sidewise — about the same as 2021. We think we’re going to get a little more growth in 2023. A lot of the growth we’re forecasting is coming from Class 8. That improvement, and there are various factors behind that, but one of them is for sure the OEMs can finally produce more vehicles so we think that can get us some incremental volume in a supply-constrained environment that we’ve been in,” he said.

“We expect to see a slowing in 2024; that’s when we think the impact of higher interest rates is going to start to bite across various sectors of the economy. We’re going to see, we think, slowing housing starts, slower growth in e-commerce, [slowing in] a number of other areas, which are going to bring down demand for new trucks in our industry,” said Divis.

He added 2024 is the bottom of the cycle and the industry will start to see a rebound in 2025 and into 2026.