MacKay & Company’s Dave Kalvelage confirmed what most in the aftermarket and dealer channels have known nearly three weeks on Monday — last year wasn’t a great one for the parts and service business.

Speaking at Heavy Duty Aftermarket Dialogue (HDAD), presented by MacKay & Company and MEMA, Kalvelage reported MacKay & Company’s final Aftermarket Index report for 2024 indicates the United States Class 6-8 truck and trailer aftermarket grew by just 1.9% last year, well below the 4.3% the company originally predicted a year ago.

And even that number was deceptive.

Kalvelage said MacKay & Company’s data now shows price rose by nearly 2.5% on average across the aftermarket last year, meaning on purely volume basis sales were actually down. The story was identical in Canada, with the market ‘growing’ by 1.9% above the border thanks solely to price.

[RELATED: Peterbilt's Skoog says time is now to prepare for next market upswing]

He added MacKay & Company’s outreach into the industry has confirmed the market softness. According to dealer and distributor responders to a November 2024 MacKay & Company survey, year-to-date parts sales were down 2.0 and 0.7% in the two channels. Within those segments Kalvelage said responders weren't universally down — 19% of dealers and 27% of distributor businesses were up — but overall sentiment was poor.

Kalvelage said the good news is MacKay & Company’s forecast for 2025 is better and there are reasons for aftermarket operations to be positive, though there is no doubt the industry is entering this year from a position of weakness.

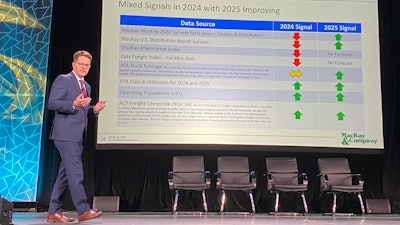

Last year was one of “mixed signals, but positives exist” to make 2025 a year of improvement, he said.

Arguably the biggest positive is the expected rebound of the freight market. ATA’s projection of 1.6% growth for truck tonnage indicates a turnaround could occur, and Kalvelage said MacKay & Company is more bullish than carriers regarding likely utilization rates for trucks and trailers in the first quarters of the year.

The new equipment market also should help the aftermarket, mostly by expanding the vehicle population. Kalvelage said MacKay & Company anticipates the Class 8 market to grow by 1% in 2025 (after falling by 10% last year) and the trailer market to rise by 5% (after a 30% drop in 2024).

Overall, he said MacKay & Company is currently projecting the U.S. aftermarket for Class 6-8 trucks and trailers to grow by 3.9% to $51.99 billion in 2025, with a five-year compound annual growth rate (CAGR) of 3.9% through 2029. MacKay’s forecast is weaker in Canada, with 2025 aftermarket demand rising by 1.8% to $6.45 billion in 2025 but improving to a 2.8% CAGR into 2029.

Bob Dieli with MacKay & Company speaks about economic business conditions at Heavy Duty Aftermarket Dialogue Monday in Grapevine, Texas.

Bob Dieli with MacKay & Company speaks about economic business conditions at Heavy Duty Aftermarket Dialogue Monday in Grapevine, Texas.

Recession risks still exist, Dieli reports

As for the economy and larger trucking industry, MacKay & Compay's Bob Dieli believes we’re still in an extended boom phase of the business cycle and therefore “recession eligible.”

Dieli cites his Truckable Economic Activity (TEA) and Enhanced Aggregate Spread (EAS) metrics for his concern. He says the former remains below well below the 5% annual growth rate that signifies good conditions for the trucking economy, while EAS remains in a dangerous zone that has, since 1970, typically predated a recession.

Dieli adds both indicators were in the same place last year at HDAD too, and 2024 played out as a soft to middling year for carriers, dealers and the aftermarket alike.

“A year ago we knew TEA was performing at a rate that was not terribly encouraging,” he said. “This year is similar.”

[RELATED: What tariffs on China, Canada and Mexico could mean for your business]

Looking outward, Dieli said the reason last year’s U.S. economy did not drop into a recession despite negative TEA and EAS metrics was multi-faceted. On one side, many businesses in the trucking sector believe they just experienced or are experiencing a recession (two quarters of negative growth). Dieli said the economy does not grow or contract linearly. Some segments are always ahead or behind the national sentiment.

On the other side, Dieli said the economy is still in the final stages of normalization post-pandemic, which has led business cycle stages to shorten or elongate in ways different than historical norms.

But Dieli also admitted EAS is not infallible. The metric’s prior success predicting a recession doesn’t guarantee a recession is coming. And if one doesn’t occur, Dieli said he’ll work hard to uncover what caused the discrepancy.

“There’s no sin in being wrong, as long as you can figure out why you were wrong,” he said.