Trailer orders still face stiff headwinds according to preliminary data for September released by FTR Transportation Intelligence and ACT Research on Friday.

FTR reported September U.S. trailer net orders rose by 75% month-over-month from a low base to 11,532 units. That's down 63% year-over-year and the lowest number for September since 2016 despite the opening of the 2025 order boards.

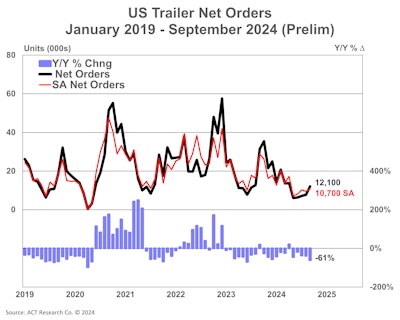

ACT showed trailer orders were up a scant 4,400 units from August to September at 12,100 units, but were down 61% over last September. Seasonal adjustment lowers the tally to 10,700 units.

[RELATED: Trailer OEMs: We’re weathering the storm together]

"Since September is the traditional start to the order season, this month's uptick was expected," says Jennifer McNealy, director of commercial vehicle market research and publications at ACT. "It's also no surprise that the data is significantly below the September 2023 intake, given the soft demand recorded throughout this year. September's data brings year-to-date 2024 U.S. trailer net orders to 101,600 units, a 34% contraction when compared to the first nine months of 2023, and puts Q3 '24 net orders at just 27,000 units, 51% lower than the same quarter last year."

FTR blamed lower numbers on lower freight demand. It says year-to-date for 2024, total trailer net orders fell 31% year-over-year averaging just 10,294 units per month. Total trailer build decreased by 11% month-over-month and 40% year-over-year in September, the company said, totaling 15,617 units. That's the lowest monthly output since July 2020, FTR says.

"Although trailer orders were weak in September, Class 8 orders slightly exceeded expectations at nearly 33,000 units for North America," says Dan Moyer, FTR senior analyst for commercial vehicles. "This divergence suggests that some fleets are prioritizing spending on new power units over trailers, possibly due to reduced profitability or shifting trade cycles."

[RELATED: Doing the math on trailer market capacity, growth potential]

ACT's McNealy says the pause button is expected to stay pressed through the rest of this year and some in the industry are expressing concern about 2025.

"The timing and size of 2025 order bookings is the wildcard," McNealy says. "Additional indicators supporting the lack of optimism include still-elevated cancellations and backlogs lower than we've seen in a decade. Despite positive momentum in the U.S. economy, lingering weak carrier profitability suggests little support for trailer orders to bolster 2025 backlogs into the end of 2024."

FTR's numbers show total net orders were below production levels and the backlog dropped to just over 82,750 units. The backlog-build ratio is now up to 5.3 months. That's about 0.6 months below the pre-2020 historical average and may induce manufacturers to slow production more.

"Higher-than-ideal trailer inventories at dealerships, lower fleet capital expenditures on trailers, and shrinking backlogs likely will put downward pressure on trailer build rates for the rest of 2024," Moyer says. "If trailer orders for 2025 don't pick up soon, some OEMs may extend or expand production cuts into next year."