Preliminary net trailer orders jumped last month but seasonal orders remain off historical averages, ACT Research and FTR report.

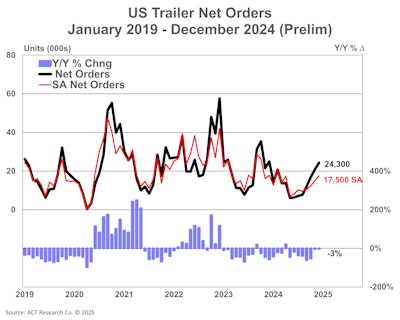

On Thursday ACT announced a preliminary order total for December of 24,300 units, up 3,500 orders from November but down 3% from December 2023. FTR's estimate was slightly higher at 25,334 units — its largest preliminary order total since October 2023 — but not large enough to overcome the slow start to the seasonal order season due to the sluggish freight market.

For the 2025 order season begun in September, FTR says orders are down 32% year over year at 18,994 units per month. ACT's estimate is similar, with the final quarter of 2024 being down 24% compared to 2023.

ACT says U.S. trailer net orders for 2024 were 163,500 units, down 31% from 2023. FTR pegs the same period at 157,085 units, down 27% year over year.

[RELATED: Two prominent Utility Trailer dealers merging]

In looking specifically at December's preliminary orders, the firms state the order data wasn't discouraging but also doesn't indicate much change in freight demand to date.

"Though past the traditional peak, we're still in the early stages of the 2025 order season, so this month's uptick was expected," says Jennifer McNealy, director of commercial vehicle market research and publications at ACT. "It's also no surprise that the data are below the December 2023 intake, given the softer demand recorded throughout this year."

FTR also notes December's orders will boost the trailer backlog. The company states total trailer production was down 10% month over month in December at 11,827 units, a relatively typical seasonal drop. However, production was down 40% from 2023 and 43% below the five-year December average and was the lowest monthly output since 2010. Total trailer production in 2024 was down 29% year over year to 223,375 units.

[RELATED: ACT: U.S. trailer backlog expands in November]

"In December, total trailer net orders significantly outpaced production, increasing backlogs to 104,725 units. The combination of rising backlogs and reduced production month-over-month pushed the backlog/build ratio up to 8.9 months — the highest level since January 2024," says Dan Moyer, senior analyst, commercial vehicles. "While this increase is largely attributed to exceptionally low production levels, it also suggests easing pressure on OEMs to further scale back production in the near term."

Moyer adds, "In 2024, North American Class 8 net orders rose 11% year over year while U.S. trailer net orders declined by 27% year over year. For-hire fleets (and, probably, private fleets too) have prioritized investments in new power units over trailers, likely driven by reduced profitability or shifts in trade cycles. This trend looks like it is continuing as North American Class 8 net orders are up 8% year over year during the 2025 order season so far while U.S. trailer net orders for the same period fell 32% year over year."

McNealy concurs.

"Notwithstanding the order improvement in Q4 2024, ACT's expectations for weak trailer demand relative to recent performance remain, as continuing weak for-hire truck market fundamentals, low used equipment valuations, relatively full dealer inventories and high interest rates impede stronger activity, especially into early 2025," she says. "An order uptick showcasing demand, or the lack thereof, depends not just on the first few months of the new order cycle, but on order volumes through Q1 2025 and beyond."