Next year will look a lot like this year in the commercial vehicle market.

The Heavy Duty Manufacturers Association (HDMA) Pulse webinar for November on Wednesday looked forward into the new year and found that, though many manufacturers are expecting a recession, they see their biggest challenges as the same problems that plagued them this year: supply chains, labor and inflation.

“Those big three of labor, supply chain and inflation are greater than any problems we see looming on the horizon, such as a recession,” says Richard Anderson, senior director of research and analysis at HDMA. “We continue to see that they are what define the experience for suppliers in the market.”

[RELATED: Monthly HDMA webinar tackles likely recession and potential impact]

There is a bright side, if it can be called that — all three are stabilizing.

“Clearly things have gotten better and are much easier to plan through,” says Jonathan Starks, CEO and CIO of FTR Transportation Intelligence, who also presented on the webinar.

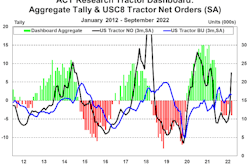

He pointed to improved Class 8 truck production as an example. Class 8 order activity remains strong and production and sales are both up and expected to stay in positive territory. Trailers and medium-duty trucks orders will also remain strong.

Starks says much of that strength comes from satisfying pent-up demand from earlier this year and 2021.

“We’ve been really disrupted during the pandemic and supply chain environment,” Starks says. Medium-duty trucks, for instance, lost the battle with passenger vehicles and Class 8 trucks for semiconductor chips. Now that supply is ramping back up, new purchases that would have occurred earlier in the year if not for the shortage are pumping up the medium-duty market.

Where the industry hits a pothole is in aftermarket upfitting. Those suppliers are hit hard by supply chains and labor shortages.

“As you move through the upfitter environment, you’re hitting production constraints,” Starks says. Medium-duty trucks are feeling it hardest, and the risk in that segment remains elevated because it’s more prone to the downside risks in the market, Starks says.

Industrial production, which had been a bright spot in the economy, is flattening out, as are freight loadings and truck utilization. All of these signs point to some kind of slowdown in 2023, Starks and Anderson agreed.

However, many manufacturers think they’ll weather the storm.

“There still remains a strong belief the existing order levels and the strength within our sector will be sufficient for us to ride out minor recessions and minor slowdowns within the economy,” Anderson says.

Looking ahead, past the fulfillment of this pandemic-driven surge of ordering, Starks sees a lingering weakness in the GDP for the goods transport sector as a real reason for heartburn. The third quarter of 2022 was lackadaisical, and that trend will reach into 2023.

“It’s not really strong enough to create demand for transportation,” Starks says. “Demand for transportation is what drives demand for trucks and trailers and all those items. This creates real concern.”

A poll of the webinar’s attendees showed most of them agreed a recession was almost inevitable in the first half of 2023. Starks says he sees economic uncertainty slowly eroding the pent-up demand driving surges in orders for trailers and vehicles, and that uncertainty clouds any forecasting much beyond the second quarter of the year.

“Order rates at the third quarter of 2023 may be more important than fourth quarter order rates,” he says. “It might give us a better indication of what the markets are looking like and how robust it is.”