While it would be an easy target, an uneven freight market is not the only reason carriers have been hesitant to expand their operations as 2024 comes to a close.

According to a September survey of carriers by CCJ, sister publication of Trucks, Parts, Service, more than half state they would like to expand their operations in the months ahead, either through acquisition, or by adding more leasing units, owner-operators or trucks with company drivers. Conversely, only 8% expect to contract.

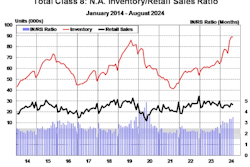

Carriers see growth opportunities in the market, and as truck tonnage starts to rise, those opportunities may only expand.

If only they could get costs in line.

When asked by CCJ to identify the biggest challenges facing their business in the coming months, the rising costs of equipment (71%) and labor (55%) were the most commonly selected issues by survey responders. The inability to hire enough drivers was next (50%), outpacing the weak freight environment (47%) and showing for a plurality of carriers, a bottom-line focus has outweighed chasing top-line growth for many operations this year.

And equipment costs are a problem for everyone.

Among fleet types, two thirds of for-hire carriers and 77% of private carriers selected it as a major challenge. Across fleet sizes, 74% carriers with 34-50 power units and 71% of carriers with more than 50 units said the same. Only smaller fleets of up to 34 units rated rising equipment costs in line with other challenges — with 50% pegging it as an issue, equal to rising labor costs but not as troubling as finding drivers (67%).

[RELATED: FTR's Starks offers better outlook for 2025 trailer space]

The good thing is growth is still a priority. Less than 10% of large fleets, private and for-hire carriers intend to contract their operations in the coming months. For carriers with less than 34 units, that number falls to zero. Businesses also are open to expanded in various ways. Nearly half of all responders (49%) would like to add trucks and drivers. And that number is well above 50% for smaller and for-hire carriers. Acquisition is another pathway some carriers (14%) are considering, while adding leasing units or owner-operators is being considered by nearly 20% of medium and large fleet operations.

Beyond equipment and employment challenges, some carriers also point to Washington as a burr in their side, with 46% rating the political climate in D.C. and regulations as a challenge. The number breaks down mostly equally across fleet segments too, with only carriers of 35 to 50 power units marking a higher level of concern.

On the flip side, integrating technology is not a major fear. Only 15% of responders rate that process as a concern — with most feature coming from larger carriers (17%).