Preliminary North American Class 8 net orders in October were 23,600 units, while Class 5-7 net orders dropped to 21,900 units, both representing lower sequential and year-over-year readings, according to ACT Research’s State of the Industry: Classes 5-8 Vehicles report.

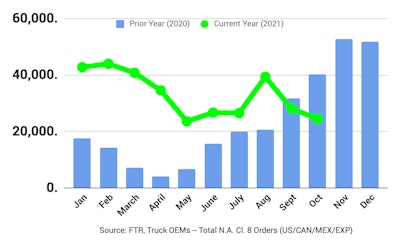

FTR reports preliminary Class 8 net orders were 24,500 units, down 12 percent from September and down 39 percent year over year. Class 8 orders have stayed within the 23,000-28,000-unit range for five of the last six months as OEMs deal with production issues. Class 8 orders now total 437,000 units for the previous 12 months.

ACT reports supply-side constraints continue to pressure new order activity.

ACT President and Senior Analyst Kenny Vieth says, “With backlogs stretching into the second half of 2022 and still no clear visibility on the easing of the everything shortage, modest October order results suggest the OEMs are taking a more cautious approach so as not to extend the cycle of customer expectations management.”

Vieth says, “Importantly, we reiterate, with critical economic and industry demand drivers at, or near, record levels, industry strength is exhibited in long backlog lead-times, rather than soft orders in October. In addition to ongoing strength in key freight-generating economic sectors and pent-up goods demand growing across a broad front, ACT’s preliminary read of the publicly traded TL carriers Q3 financial results shows net profits approaching best-ever levels.”

FTR reports OEMs are still finding it difficult to manage orders that will not get built this year due to component shortages. Production rates in the first quarter remain uncertain because of supply chain difficulties and worker availability. OEMs continue to be careful not to overbook fleet orders for the first half of 2022.

Don Ake, FTR vice president of commercial vehicles says, “The OEMs are having tremendous difficulty planning production for Q1. Unfinished orders are rolling over from 2021 and there are fleets placing new orders for 2022 delivery. All these fleets are desperate for new trucks and the challenge for the OEMs is to book the maximum production possible without excessive overbooking.

“The OEMs are using different methods in managing the backlog. Some are canceling 2021 orders and rebooking those orders in 2022, sometimes at higher prices, as commodity and other costs remain elevated. Others are only booking a limited number of orders every month,” Ake says.

“It is interesting that the order rate has been basically tracking the production rate since May, with a couple of exceptions. It indicates that the market is essentially frozen in this range of around 22,000-26,000 trucks. Without the clogged supply chain, production would be significantly higher, and orders would be elevated also.”

Complete industry data for October, including final order numbers, will be published by ACT Research and FTR later this month.