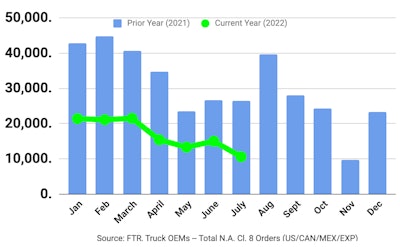

North American Class 8 net orders for July fell to their lowest level since November 2021, according to FTR, which is reporting preliminary orders at 10,600 units. ACT Research reports July orders at 11,400 units.

Order activity was the weakest for the month of July since 2019, down 33 percent from June and down 60 percent year over year. Class 8 orders have now totaled 244,000 for the past 12 months, according to FTR.

OEMs have essentially run out of build slots for 2022 and are not yet entering orders for 2023. The continued supply chain disruptions are limiting OEM output in 2022 and the fluctuating cost of materials and components has caused delays in confirming orders for shipment next year. Demand for new trucks remains strong, FTR reports.

“Orders, though paltry, met expectations since OEMs have filled almost all available build slots this year. July is typically the weakest order month of the year, so it is no surprise orders dipped to around 10,000 units. Fleets continue to shop around, looking for available trucks, but they are becoming increasingly difficult to find. The supply chain is improving very slowly, but not nearly enough to meet demand,” says Don Ake, FTR vice president of commercial vehicles.

“It's like when popular concert seats are sold out, you get no sales the next day. Class 8 trucks are popular and in scarce supply in 2022. The OEMs just don’t have the capacity to meet the high demand this year. OEMs could increase production by about 10 percent over the current rate if they could get the parts, but the supply chain remains clogged,” Ake says.

“Despite the economic uncertainty, demand for new trucks is expected to remain robust in 2023. Freight is still forecast to grow at a steady clip. When booking commences for 2023, possibly as early as September, Class 8 orders could reach record heights,” he adds.

ACT Vice President and Senior Analyst Eric Crawford says, “Do we think July’s weak orders represent the end of healthy demand? Perhaps. Recent spot rate weakness, and our expectation that a freight recession is inbound, would suggest yes.”

That said, Class 8 backlogs stretching into 2023, ongoing supply-chain issues, albeit easing somewhat, and inflationary cost pressures leave the OEMs in no rush to open order boards for 2023,” according to Crawford.

“In light of this confluence of factors, plus typically challenged seasonality in Q3, we hesitate to extrapolate too much from a datapoint that could prove to be an outlier. To be sure, though, it is a datapoint that warrants increased vigilance going forward,” he says.

Crawford adds, “Per the backlog analysis and OEM build plans in ACT’s July State of the Industry: NA Classes 5-8 Vehicles report, the 2022 backlog was oversubscribed, with 39,000 more orders scheduled to be built than build slots available, at the end of June, and June cancellations were negligible.”

ACT is reporting Classes 5-7 net orders at 13,500 units.

“July demand for medium-duty vehicles was similarly challenged, representing the lowest seasonally adjusted total since the pandemic — likely, at least in part, evidence of the shift in consumer spending from goods to services,” Crawford says.