The last two years won’t be looked back on fondly for commercial truck and trailer dealers, but they might ultimately prove useful for what they taught dealer businesses about their profitability and operational effectiveness.

Strong new equipment sales paper over a lot of inefficiencies. But when orders and deliveries unexpectedly subside, expandable fixed operations departments, lease and rental acumen, tech-based resource optimization and, as always, customer expertise, become essential to avoiding P&L nightmares.

And with 70% of dealer responders to a recent Trucks, Parts, Service reader survey stating they expect dealer revenues to rise year over year in 2026, channel sentiment indicates the lessons of 2024 and 2025 are already learned.

2025: The year the recovery never came

Since the freight recession began in 2023 and dealer revenues started to fall, dealer optimism has never crept higher than it did in January 2025.

The market was hardly booming — 33% of dealer responders to the recent TPS reader survey reported their businesses were down year over year in 2024 with another 9% flat — but truck orders displayed consistency with some growth in the final months of 2024 and the election of President Donald J. Trump created excitement for the economy.

Unfortunately, optimism alone couldn’t turn things around.

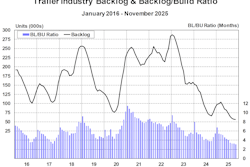

Freight rose in February as shippers raced to import goods ahead of new tariffs but cratered in the months that followed. Trade uncertainty, which materialized almost immediately after Inauguration Day, continued to weaken investor confidence all spring, and by June truck orders had fallen to a 16-year low. Trailer orders faltered a month later.

June did see Trump’s revocation of the EPA waivers used by California’s Air Resources Board (CARB) for its sales-prohibitive Omnibus and Advanced Clean Trucks rules, but it also saw the expansion of steel and aluminum tariffs.

In both equipment segments, sales have yet to recover.

[RELATED: We’ve also asked aftermarket operations and your supplier partners about how they expect to fare in 2026.]

The silver lining, if one existed, was dealers already had a year-plus of experience in a depressed market.

“This year business has been about what was expected,” Chris Marsh, executive vice president of new and used sales at Advantage Truck Group, told TPS in late 2025. “We continue to be in [a] freight recession, which cripples on-highway users,” he added, while regulations in his region also kneecapped sales potential for all equipment.

Joe Selking, president at Selking International, agreed.

He told TPS in December his company had expected “slightly higher” sales in 2025 before economic and tariff uncertainty weakened the market. Fortunately, Selking was able to pivot its focus into other areas, setting a record in used trucks sold and growing its leasing business.

The company made corresponding investments too, he said, adding a used salesperson and rental agent to maximize the revenue potential of those stronger areas.

“Freight rates [were] down, customer confidence is down, concerns about tariffs and used values are down,” Selking said. “Customers were more comfortable buying used and/or leasing.”

Advantage took similar actions.

Marsh said vocational remains the dealer group’s strongest sales segment so its team spent 2025 prioritizing vocational customers, and “continually working to further diversify our business with new customers along with vocational opportunities.”

In its service shops, which also saw mixed results, Advantage Executive Vice President of Service Operations Chris Pentedemos said his team worked hard to “keep staffing levels up to ensure work is turned quickly” in its strongest markets.

Vocational was a point of emphasis at Rush Enterprises too, President, Chairman and CEO Rusty Rush said during a press conference last month at the company’s Tech Skills Rodeo.

“The refuse business, we work on that segment more than anybody,” he said.

The channel’s flexibility could be seen in its 2025 results. While most dealers revealed in the recent TPS reader survey their businesses would come up short of their 2025 business projections, results were better when overlayed against 2024.

Equally impressive, 27% of dealer responders reported expanding their facilities in 2025 while another 27% considered expansion; only 3% of dealers contracted their operation.

But the channel’s perseverance wasn’t without casualties. Nearly 40% of TPS survey dealer responders reported their personnel levels fell in 2025. Another 12% grew, but did not exceed their highest point from 2024.

Could 2026 finally turns things around?

Among TPS survey dealer responders, this is a definite maybe. Reasonable confidence exists.

As mentioned previously, 70% of responders expect dealer revenues to improve in 2026. Almost all (64%) expect an improvement of 2-10%, but after the past two years, even mild growth would be welcome.

Rush believes the last quarter and current quarter are the “two toughest quarters we’re going to have” as the industry delivers 2025’s weak summer order totals to customers. He’s hopeful carrier equilibrium follows in Q2, which combined with an amended and finalized EPA 2027 NOx rule could kickstart a willingness from on-highway carriers to start placing orders again.

[RELATED: Rusty Rush cites overcapacity as thorn in truck sales turnaround]

Marsh offers a similar assessment, stating he expects a flat first quarter with “upticks beginning in Q2 through the end of the year,” and said his customers appear “conservatively optimistic.”

Pentedemos also expects an increase in service, citing the aging truck population.

“Trucks are aging and with new unit sales down repairs will be needed and those trucks needing repairs will be out of warranty,” he said.

“I have an optimistic outlook for 2026,” added Selking. “I think consumer confidence will increase, tariff concerns will decrease, interest rates will go lower, hopefully inflation will normalize and the business climate will improve.”

Michael Ramian, Advantage’s executive vice president of parts operations, believes 2026 parts sales will follow the template laid in 2024 and 2025, with inconsistency month to month and certain customer segments, regions and product categories outperforming others.

He said Advantage’s parts business picked up in the latter half of 2025 so there’s hope that continues. His team has been focused on “increased parts marketing and strategic buying” to maximize its strongest areas.

Dealers also believe in their internal abilities to outpace the market, wherever it goes.

More than 80% of TPS survey dealer responders expect to grow by more than 2% in 2026 against 2025 — 67% up 2-10% and 15% by more than 10%. Some of that optimism could be due to comparing against flagging 2025 revenues, but those numbers are noticeably higher than their market wide predictions. Additionally while 18% of dealers expect the industry to be flat, only 9% expect that for their business.

Yet forecasting 2026 is not without its challenges. The freight recession is approaching a record-setting length but that alone doesn’t mean a turnaround is imminent.

As such, equipment sales predictions for the year run the gamut. Most dealers (70%) believe trailer sales will be steady but there’s no consensus for new and used truck sales.

There’s also the problem of outside influences. Trucking is beholden to economic and political activity.

“Political unrest will lead to continued wait and see focus of our customers,” one survey responder stated.

“The inconsistency of tariffs make it hard to quote units for long-term delivery,” said another. “On a $150,000 truck a net tariff of 3.5% equates to over $5,000. On a 50-truck deal that’s over $250,000. It can easily make a customer cancel the order. For an owner-operator running one unit, they will often back out of the deal and look for a unit in stock that is not affected by the tariff.”

Whiteford Kenworth Vice President R.C. Euler also cited tariffs as hardest part of 2025 for his business, and told TPS in November his expectations for 2026 “were in line with what we are experiencing 2025” due to uncertainty in its customer base.

Survey sentiment was similar.

One responder stated “the economic climate across the country” as the biggest issue facing dealers in 2026. Another said “tariffs, taxes and supply chain,” while a third wrote “too many trucks parked and no demand for new truck purchases.”

And parking of too many trucks is a real problem. While rightsizing capacity requires the removal of some trucks from active use, fewer trucks on the road reduces parts and service opportunities.

“Theoretically when you don’t buy more new trucks you should have more maintenance, but there’s also a lot of stuff being parked,” Rush said. “Theory doesn’t drive reality. You’re naturally going to be a little more frugal in your spend.

He continued, “Maybe you extend your oil changes. Maybe you don’t fix that fender. Or if you have other trucks you don’t use, you cannibalize them. If your revenue goes down, you become more diligent in your expenditures.”

Like carriers, dealers have been doing that for two years.

“Reducing expenses as best we can” has been a priority at Whiteford, Euler said, adding stabilization on the trade front and some ‘trickle down’ support from OEMs would be helpful for dealers “until we come out on the other side.”

Selking also believes trade stability would be helpful, particularly for customers desperate for normalcy. He said that’s where his business will focus in 2026.

“People are tired of hearing about supply chain issues, allocation, downward pressure, inflation and tariffs. They just want normal. Therefore, we are working hard to present normal,” he said.

This is Part II of the Trucks, Parts, Service biennial state of the industry report, featuring insights from aftermarket, dealer and commercial vehicle supplier experts.

To read Part I addressing expectations for the independent aftermarket, CLICK HERE. To read Part III with insights from industry suppliers, CLICK HERE.