Optimism is in rare supply as 2025 comes to a close, but there are some rays of hope. Suppliers, like much of the aftermarket, looked for more of a freight recovery this year and instead got more uncertainty and anxiety along with continued low freight rates.

MEMA surveyed medium- and heavy-duty suppliers in the fourth quarter of 2025 and found the segment sees positive albeit slow growth ahead despite a great deal of uncertainty surrounding trade and regulatory policy. Joe Zaciek, director of research and industry analysis, says the numbers have been improving as the year moves on and a growing number of members say they’re optimistic about the next 12 months.

By and large, Trucks, Parts, Service’s own recent survey and interviews show, any thoughts of recovery are cautious and creeping, but they are there.

An abysmal 2025 for equipment orders

About a quarter of TPS respondents said their 2025 performed how they expected when surveyed in November. But a third said their predictions for 2025 were slightly off and the company ended the year 2-10% below expectations. Another quarter said it was even worse and 2025 was significantly below, more than 10% below, projections.

[RELATED: We’ve also asked dealers and aftermarket operations about how they expect to fare in 2026.]

“We entered 2025 anticipating stronger demand, expecting customers to make early purchasing decisions ahead of the 2027 emissions regulations,” says Amanda Phillips, executive director for Cummins’ North America on-highway OEM engine sales. “However, tariffs, freight costs and regulatory uncertainty created headwinds that tempered those expectations.”

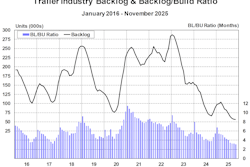

Randy Flanagan, vice president of sales — trailer for SAF-Holland, says earlier in the year, vocational trucks were strong and propped up sales at OEMs. But when that demand leveled off, the tractor side was still in low gear, throwing off sales. FTR Transportation Intelligence says Class 8 net orders are down 32% year to date over 2024.

“We expect 2026 to be another weak build year,” Flanagan adds. “As long as freight and rates lay low, fleets will not have the funds available to buy. Even with the emissions mandate looming, changing or going away, time is running out and the horizon for truck purchases still is not materializing.”

Improving 2026 for suppliers

For this year, 66% of TPS respondents said in November they’re expecting either slightly higher (2-10%) or significantly higher (more than 10%) revenue next year, even in the face of a years-long freight recession. And that’s largely because of respondents’ close relationships with their customers.

Dave McCleave, director of the aftermarket for Hendrickson, says his teams will continue to be problem solvers, staying relevant and bringing their customers valuable educational resources.

“Be the resource for first call with the customer base,” he says.

At Cummins, Phillips says they pride themselves on maintaining a consultative relationships with its customers.

“Our teams focus on understanding customer needs and providing solutions that create value,” she says. “With a vast network of locations, customers can rely on our presence and support wherever they operate.”

SAF-Holland thinks trailer sales will bounce back after years of neglect but until then, it’s improving its manufacturing processes and working to improve sourcing to minimize exposure to tariffs. FTR Vice President of Trucking Avery Vise says as of the end of 2025, once exceptions and exclusions are stripped out of tariff regulations, the impact overall on equipment is about 9%, and the MEMA survey backs that up.

Tariffs are a challenge for suppliers, with several citing the trade policy directly in their comments on the TPS survey and 47% of TPS respondents stating general business and economic conditions, including tariffs, remain their top concern.

“This is obviously causing a tremendous amount of pain for our members,” MEMA’s Zaciek says. He says there may be some U.S.-Mexico-Canada Agreement exceptions to provide relief for medium- and heavy-duty equipment dealers and manufacturers, but there will still be a pinch point if tariffs stay in effect.

Other concerns cited by TPS respondents include:

- The merger between FleetPride and Truck Pro. “They have significant overlap in some markets,” one person says. “The national fleet just lost a source,” another writes.

- Interest rates. Even though the Fed recently lowered rates, the cost of capital continues to be higher than it has been in several years.

- A lack of employees across the industry, including the driver shortage.

- Raw material prices and increases in production costs.

Employment and investment outlook

Around a third of TPS supplier respondents in November said their total personnel fell in 2025. Another 47% said they had no net change in personnel. Just 11% said their total personnel went up.

The level of job creation in manufacturing is important to the Trump administration, Zaciek says, and even so, since tariffs started, MEMA’s members are reporting shrinking workforces. The organization’s survey showed commercial vehicle OEMs lost 33% of its U.S. production employee headcount while industry-wide (automotive and commercial vehicles), Tier 1 and Tier 2+ suppliers were down 23%.

The good news in the MEMA survey is commercial vehicle OEMs are neutral on investment. Zaciek calls more investment a “very positive signal” and says the expectation is that manufacturers will start rehiring and bringing on new production employees.

“It does seem like we’re coming out of the investment push-back,” he says.

That investment may start as soon as freight rates start their long crawl from the bottom.

“We watch freight rates very closely,” Flanagan says. “Freight = profits = purchases.”

Hendrickson’s McCleave says freight drives equipment build and component replacement. The company also keeps an eye on equipment leasing.

“If equipment leasing picks up, it is a possible indicator that freight hauls are beginning to increase, additional hauling capacity is needed, thus eventually driving part replacement demand,” he says. “The opposite is also true. If leased equipment begins to decline without offsetting new equipment purchases.”

Diversity of product offerings

About half of TPS supplier respondents said they expanded product lines in 2025 and, notably, just 8% reduced product lines. This may help suppliers continue to be problem-solvers for their customers.

Cummins says it’s focused on solutions that help customers reduce operating costs as well as emissions, even with the uncertainty regarding EPA regulations.

[RELATED: How Rush remains engaged with truck buyers despite flagging market]

“EPA’s direction on the 2027 low NOx rule is an important step in advancing regulatory certainty, and we will continue to work toward our shared goal of fostering American competitiveness as the agency finalizes the rule,” Phillips says.

More solutions also may increase profits not only for suppliers but also for fleets.

“This is an excellent time to present to the fleets new products, systems and technologies that offer real ROI opportunities,” SAF-Holland’s Flanagan says. “We also are working with all our OEM customers on driving out costs and preparing for the next upturn to be able to support demand.”

SAF-Holland says it is seeing interest in smart trailers and sensors that can help fleets optimize intervals and avoid costly repairs. At Cummins, it is seeing “significant interest” in products that reduce the environmental impacts of commercial vehicles.

“There is not a single path to decarbonization,” Phillips says. “This market has huge variation in applications. No one solution will meet the needs of everyone. … When certain markets and applications are ready for alternative technologies, we are ready to meet those needs.

Getting ready for brighter days

With some glimmers of expansion in the marketplace, such as investment expectations climbing out of the negative, some suppliers are looking ahead to some expansion in the next 12 months.

“We’ve invested more than a billion dollars into our manufacturing sites to better serve our customers and reinforce our commitment to innovating for their needs today and tomorrow,” Phillips says. “Looking to 2026, we recognize the primary concerns are the combination of tariffs and transitioning to 2027 products. We’re working closely with customers and across the supply chain to encourage early planning.”

McCleave is looking to artificial intelligence (AI) to create efficiencies in business processes and also monitoring the Right to Repair Act and environmental regulations.

“Even if all the regulatory initiatives may not impact us directly, there could be indirect impacts that could shape various go-to-market strategies,” he says.

Vise sees some reason for optimism when looking at publicly traded carriers’ profits. Recent data shows revenues for the trucking sector is up 4.2% year over year.

“That’s some strong performance,” he says. “It’s certainly something to be encouraged if you care about carrier health.”

Eventually, Vise says, the lack of buying in 2025 and advancing age of equipment in service may interfere with capacity and force purchases.

“If you play this out over time, this lower level of demand is potentially going to have implications in late 2026 and 2027 and beyond,” he says, adding declines in production should worry shippers and fleets alike as it could limit equipment availability. “These are meaningful moves. This is a big deal if we have disruptions on both labor and equipment.”

This is Part III of the Trucks, Parts, Service biennial state of the industry report, featuring insights from aftermarket, dealer and commercial vehicle supplier experts.

To read Part I addressing expectations for the independent aftermarket, CLICK HERE. To read Part II for insights from the dealer channel, CLICK HERE.