This year started off with wild swings in economic policy, but those are starting to moderate, if only a little, FTR Transportation Intelligence says Thursday in its mid-year State of Freight webinar.

“It’s been more stable in recent months,” Joseph Towers, senior analyst for rail, says. “But it still isn’t a very clear environment. This makes it very difficult for businesses to make decisions.”

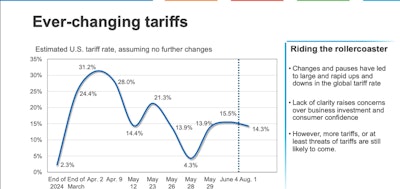

FTR predicts an average tariff rate of around 14.3% going into the later half of the year, but Avery Vise, vice president for trucking, says that’s likely low given another round of threats from Washington.

“It’s likely to be a floor rather than a ceiling,” Vise says, with forecasts assuming a global average tariff rate of about 18%. Vise says the company’s forecasts also expect rising inflation and a lowering of interest rates — “the most iffy of our assumptions” — toward the end of the year.

Manufacturing had a strong first quarter, as did the goods transport sector, data shows. Vise says the first-quarter numbers for goods transport shot up 19% quarter-over-quarter as companies grabbed up goods before tariffs took effect.

“But we do expect payback,” Vise warns, outlining a forecast with both categories slipping into the negative before a 2026 recovery. Overall, however, the strength of the first quarter will mean moderate gains year-over-year, he says.

Freight rates, which have been bouncing around the bottom for a while, had a surprise bump in the last week, Vise says, but he’s hesitant to call it in inflection point for the market.

“Is this the turn we’ve been looking for?” he says, possibly, but not probably, he cautions, saying he won’t extrapolate much from one week of good data and needs to see more weeks of increase to call it a trend.

Much like manufacturing and goods transport indicators, Vise says total truck loadings saw a strong first quarter followed by a weaker rest of the year and a mild recovery into 2026. Dry van will be negative year-over-year, with stronger tank and flatbed sectors.

Truck utilization numbers are also a little higher than the historical average with softness in the forecast, Vise says, citing slowing freight demand, the impact of English language proficiency regulations and a surge in insurance premiums as particular problems to watch for.

Less than 2% growth is forecast in total truckload contract rates, he says, which is not enough to offset inflation. Should the forecast hold true, Vise says he expects to see downsizing.

“This is a positive, technically, but from the carrier perspective, it’s not all that positive,” he says.

Class 8 truck orders remain abysmal amid record inventories, and Vise attributes that to a number of factors, such as tariffs, the sluggish freight market and uncertainty surrounding emissions regulations. The low number of orders could set the stage for tighter capacity as the market recovers he says, but there are trucks available even if they don’t match buyers’ preferences.

“If there is a need for trucks, at least for a little while, trucks will be available,” Vise says. He expects the reduction in orders to continue at least through the fall, though there are some possibilities the market may reverse similar to what happened in 2017 with the passage of the taxes the 2025 Big Beautiful Bill made permanent.

“This is more about preventing a downside than creating an upside,” he says. “None of that is going to matter unless we have more freight. That’s the bottom line. We have to have more freight.”