Class 8 truck orders shot up over the last few months, FTR analysts said Thursday on a State of Freight webinar, as the EPA provided clarification on regulatory matters and tariffs proved to be less impactful than originally feared.

"Net orders were subdued through November," senior analyst Dan Moyer says, then, in December "shot up like the moon rocket." As of March, net orders are up 137% year over year and it may be a sustainable march upwards as freight fundamentals, such as rates and manufacturing outputs, continue to improve.

[RELATED: Mapping the Market: U.S. carrier, equipment levels steadied in Q1]

Trucking Vice President Avery Vise says manufacturing is in positive territory; not strong, but still positive.

"It's OK," he says. "It is improving, but it still not overly robust."

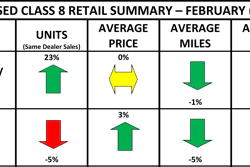

Rates are going up, largely in response to volatility in diesel prices, but also in the tightening of capacity. Vise says the actual all-in spot rate is the highest its been since 2022. Flatbed rates, driven by data center construction and other specialized areas, are still high and rising.

The contraction in capacity plays out in active Class 8 trucks data, which is at its lowest level of active drivers since the disruption of the pandemic. It's expected to start climbing as data supports an increase in trucks, which, in turn will stall out active utilization rates, a volatile statistic in recent years.

Jonathan Starks, FTR's CEO, says the addition of new vehicles into the marketplace is no longer part of the replacement cycle and will result in added capacity. This trucking recovery is not playing out on the normal pattern, he says. Usually, truck production and sales likes to move in a more sustainable trajectory, not the sharp peaks and valleys seen in FTR's charts.

[RELATED: Class 8 orders neared 50,000 units in February, ACT Research says]

Moyer says some of the spike in Class 8 orders drew from high levels of inventory and there's always the chance that some orders are just holding build spots for hopeful carriers. Still, he and FTR are forecasting build rates to rise by the third quarter as fleets begin to prepare for 2027 NOx regulations. He also pointed out there may also be a cap to what OEMs can realistically produce, particularly with the new weight of tariffs and United States-Mexico-Canada trade agreement negotiations looming.

"You don't move all of your production back to the U.S. overnight," Moyer says. "Even if you're bringing back production, you eventually reach a cap to what can be produced in the U.S. Definitely, Mexico will be an increasing percentage of North American production to support higher demand."

That, in turn, may ratchet up tariff cost impacts, but still, it won't be as high as initially suspected. With USMCA, the economic impact is about 4.8% on the average Class 8 vehicle, FTR says.

Another potential cost impact comes from 2027 NOx regulations from the EPA. Those won't be completely clarified until later this month, the agency says, but as it stands, Moyer says the rough estimate now is $10-$15,000 per truck, down from $20-$30,000.