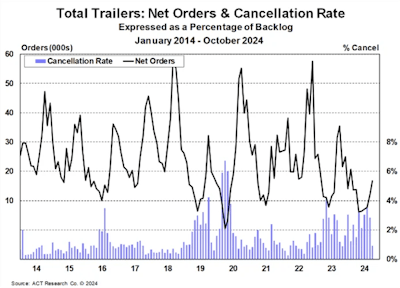

ACT Research announced final October net trailer orders, at 16,900 units Monday, up 40% from September, but 52% below the level accepted in October 2023.

Cancelations were down, however, below 1% of backlog, for the first time since November 2023. That rate has oscillated at elevated levels, between 1.2% and 3.6% throughout 2024, says Jennifer McNealy, director, CV market research and publications at ACT Research.

“In the present environment, the challenge is that while quotation activity is happening, order placement remains tepid to date. Data continue to tell the story of macro-facing industry segments being particularly hard hit, with the industry traversing a much more competitive landscape than the past several years,” she says. “Simultaneously, strong Class 8 equipment purchases continue to oversupply the market, thereby dampening for-hire freight rates and limiting capex for new trailers.”

[RELATED: NTDA launching political action committee]

What will it take for the trailer industry to see a return to normal? McNealy says the market took a key step forward earlier this month.

“Trailer manufacturers have indicated that one of the pivot points needed to get the sales environment back on track was to move beyond the U.S. presidential election. While that milestone has been reached, the ramifications of that event remain unknown, and there are several other signposts that have not yet been realized, including freight demand/rate improvements, interest rates (lower capital costs), used trailer valuations, improved consumer confidence, and better industrial activity,” she says.