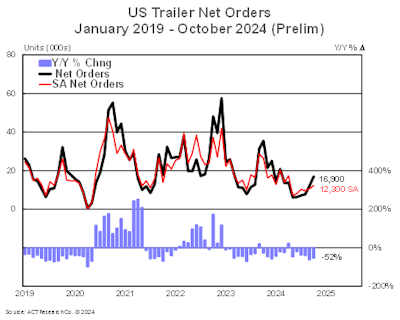

Preliminary trailer orders leapt up last month, jumping 4,800 units to 16,900 units, ACT Research reported Friday. FTR pegged the orders as up 34% from September to 15,970 units. Despite the month-over-month bump, the totals were still down 52% and 55%, respectively, from 2023, the companies state.

ACT says its seasonal adjustment (SA) at this point in the annual order cycle lowers October’s tally to 12,300 units, which sits 16% above September’s seasonally adjusted intake. For the year, trailer orders total 118,300 units, down 37.5% from the same period last year. FTR adds the October estimate is the lowest since it began tracking trailer data in 2013.

“Since we’re still in the early stages of the traditional start to the order season, this month’s uptick was expected. It’s also no surprise that the data is significantly below the October 2023 intake, given the soft demand recorded throughout this year,” says Jennifer McNealy, director, CV market research and publications at ACT Research. “Despite the sequential order improvement, October data continue to bear witness to our expectations of weaker trailer demand relative to recent performance, as continuing weak for-hire truck market fundamentals, low used equipment valuations and already-filled dealer inventories impede stronger activity, especially into early 2025.”

[RELATED: Mexican trailer business on the rise]

FTR reports its trailer net orders for the year to date (YTD) fell 36% year over year to 108,977 units, an average of just 10,898 units per month. Total trailer build rose 8% month over month in October to 16,603 units, aligning with typical seasonal patterns, but was down 38% from 2023. This output is 34% below the five-year average for October and marks the second-lowest monthly production level since August 2020, the company says.

“With the launch of the 2025 order season, North American Class 8 net orders increased 6% year over year in September-October 2024 while U.S. trailer net orders dropped by 58% year over year during the same period,” says FTR Senior Analyst of Commercial Vehicles Dan Moyer. “The steep decline in trailer demand is largely due to fleets prioritizing investments in new power units over trailers, likely influenced by reduced profitability or shifts in trade cycles. Some fleets might also have been postponing trailer orders until after the November elections or in hopes of lower trailer prices.”

FTR's data also shows October total trailer net orders were slightly below total production, reducing backlogs by 1,017 units to 82,089 units. Higher month over month production and lower backlogs pulled the backlog/build ratio down to 4.9 months, the lowest since June 2020 and about a month below the pre-2020 average. This result indicates mounting pressure on OEMs to scale back production in the near term, the company says.

[RELATED: Used truck market turnaround should come in early 2025]

Moyer says, “Slightly elevated trailer inventories, reduced fleet spending, and shrinking backlogs are expected to pressure trailer production levels through the rest of 2024. If 2025 trailer orders fail to rebound soon, some OEMs may need to extend or deepen production cuts into next year.”

“An order uptick showcasing demand, or the lack thereof, depends not just on the first two months of the new order cycle, but at least on order volumes through January 2025,” adds McNealy. “Industry anecdotes suggest that the lack of optimism continues, based on lower backlogs than we’ve seen in a decade. Despite positive momentum in the U.S. economy, lingering weak carrier profitability suggests little support for trailer orders heading into 2025.”

“Slightly elevated trailer inventories, reduced fleet spending, and shrinking backlogs are expected to pressure trailer production levels through the rest of 2024. If 2025 trailer orders fail to rebound soon, some OEMs may need to extend or deepen production cuts into next year.”

Used volumes continue to rise

In that space, the company says preliminary same dealer retail sales volume were up 29% in October.

“Following the September preliminary release’s high-side surprise (+11%), final Class 8 same dealer used truck retail sales volumes declined 6.2%. We advised that the variation in participants could and did lead to different results,” says to Steve Tam, vice president ACT Research. “October Class 8 same dealer used truck retail sales volume growth appears to be shaping up for a similar scenario. Seasonality called for a decrease of about 3% month over month.”