Used truck prices and volumes were mostly stable in the auction market last month while the retail sector saw an uptick in sales, J.D. Power reported Thursday in its June 2024 Commercial Truck Guidelines report.

Within the auction space, the volume of Class 8 sleeper tractors in May was very similar to April, which is typical. J.D. Power says on a mileage-adjusted basis, pricing for these trucks changed very little. The market was more evenly weighted between low, average and high-mileage trucks than any other month this year.

- Model year (MY) 2021: $46,797; $3,376 (6.7%) lower than April

- MY 2020: $35,246; $2,813 (8.7%) higher than April

- MY 2019: $28,698; $1,949 (7.3%) higher than April

- MY 2018: $29,083; $9,782 (50.7%) higher than April

J.D. Power states the unusual jump in average price of model-year 2018 trucks was due mainly to a more favorable mix of specs in the dataset, which is unusual to see month over month and, therefore, not a parameter for which it adjusts. Otherwise, in May, selling prices for 4- to 6-year-old sleepers were essentially unchanged for a third consecutive month, bringing 1.3% more money on average than April, and 1.8% more than March. Values for this age group are still about 7% lower than the strong pre-pandemic period of 2018 in nominal figures, or about 23% lower if adjusted for inflation.

[RELATED: Used truck volumes buck seasonal trend, leap upward in May]

J.D. Power adds current pricing is about 43% higher than the last market nadir in late 2019, or about 18% higher if adjusted for inflation. Depreciation in 2024 is averaging 4.3% per month. Pricing is now halfway between 2018 (strong) and 2019 (weak) levels in real numbers.

"Capacity utilization still points to an oversupplied market. Spot and contract freight rates remain below 2019 in real numbers, although spot appears to have stabilized," the company says. "May results, like April, are somewhat stronger than expected. For now, buyers seem content with pricing in the current supply/demand environment."

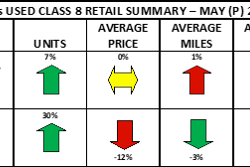

J.D. Power states the average sleeper tractor retailed in May 2024 was 71 months old, had 438,344 miles and brought $59,760. Compared with April, this average sleeper was one month newer, had 13,912 (3.1%) fewer miles and brought $745 (1.2%) less money. Compared with May 2023, this average sleeper was one month newer, had 32,888 (7.0%) fewer miles and brought $12,304 (17.1%) less money, the company says.

Within its most common cohort of late-model trucks, pricing was as follows:

- MY 2023: $130,115 $7,263 (5.3%) lower than April

- MY 2022: $94,882; $485 (0.5%) lower than April

- MY 2021: $71,885; $2,658 (3.6%) lower than April

- MY 2020: $52,415; $3,453 (6.2%) lower than April

- MY 2019: $42,809; $715 (1.6%) lower than April

- MY 2018: $31,253; $3,020 (8.8%) lower than April

The company states 3- to 5-year-old sleeper tractors brought 2.9% less money in May 2024 than April, and 16.9% less than May 2023.

"Late-model sleepers are bringing money comparable to the last strong pre-pandemic period of early 2019 in nominal dollars, or about 19% less when adjusted for inflation," J.D. Power states. "Compared with the last weak pre-pandemic period, late-model sleeper values are running 24% higher in nominal dollars or essentially equal money in real dollars. Depreciation in 2024 is averaging 2.8% per month, which is historically typical."

J.D. Power also reports its sample set of daycabs saw a substantial decrease in selling price in May compared with April, which was unexpected and illogical. For now, we attribute the decline to an unfavorable mix of models and specs in the dataset, and we expect June’s result to recover this loss. Specifically, late-model daycabs brought 15.7% less money in May than April. Compared with May 2023, this segment brought 17.4% less money. May’s unusual result pushed this year’s average monthly depreciation to 3.2%, J.D Power says.

[RELATED: Peterbilt adds optional warranty option for Red Oval trucks]

As for movement, May’s retail sales volume recovered most of the loss from April, averaging 2.5 trucks per rooftop. The company says this figure is 0.4 truck higher than April, and in line with volumes seen since the market correction began in mid-2022. At this point, J.D. Power states it consider April’s drop an anomaly.

Looking forward, J.D. Power's analysis is cautious yet hopeful.

"Market trends that begin in the auction channel generally take about three months to show up in the retail channel. If that rule of thumb holds true, retail pricing should be stabilizing as we speak," the company says. "However, the market in general is still defined by oversupply, and the traditional retail buyer is facing a difficult lending and insurance environment. The worst of the correction is behind us, but pricing pressure is still more downward than upward."

For more information, and to read the entirety of this month’s report, please CLICK HERE.