A boost in retail volumes in March didn’t impact Class 8 retail used truck pricing but did cascade to a reduction in volumes and pricing in the auction sector, J.D. Power announced this week in its April 2026 Commercial Truck Guidelines report.

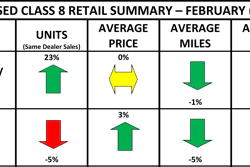

After a huge surge in volume in the auction space in February, volumes were down an astonishing 53% month over month and 62% year over year. Pricing fell too, down 7.1% against February and 11.6% against 2025. Overall, J.D. Power reports monthly depreciation in the auction space of 4.8% year-to-date, with volumes now down 4.2% over the first quarter of the year.

In releasing its data, J.D. Power states the sudden drying up of the auction space indicates units are “increasingly being absorbed through retail and wholesale channels rather than the auction lane — a positive structural shift for overall market pricing, though elevated fuel prices tied to ongoing geopolitical conflict in the Middle East remain a meaningful headwind to sustained momentum heading into Q2.”

Within those other channels, the market was much firmer.

In the wholesale space, sales per rooftop were up 0.1 against February but down 0.2 trucks against March 2025. Year-to-date volumes are flat. Pricing was mixed, up 3.5% month over month but down 2.8% against 2025 and 3.6% year-to-date 2026 against 2025. Wholesale depreciation is 3.3% year-to-date.

[RELATED: TPS survey shows dealers scuffle while aftermarket rebound continues]

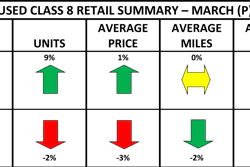

The retail market volume boom was evident in all J.D. Power data sets. Sales per rooftop were up 1.2 trucks month over month, 2.1 trucks year over year and are now up 1.7 trucks year-to-date against 2025. The company says the month-over-month gain shown in March also drives retail volumes to best level in nearly five years.

J.D. Power believes the influx signals “renewed buyer confidence in the freight environment; a combination of stable pricing and rising demand that points to genuine strengthening in the retail channel rather than a temporary distortion.”

And pricing was strong even with the higher volumes, up 0.8% month over month (though down 4.8% against March 2025). J.D. Power reports retail prices are up 0.7% year-to-date, with monthly depreciation steady at 2.0%.

“Overall, March’s market data was encouraging,” J.D. Power states. “Retail results were the standout, with the substantial increase in sales volume combined with stable pricing suggesting that buyers are more confident about their prospects in the freight environment.

“On the wholesale side, higher pricing suggests that dealers are more actively looking for specific inventory. Auction volume and pricing were the exceptions to the positive trends, but downward movement in that channel may mean more inventory is being sold through retail and wholesale channels.”

The company states the primary headwind to increased positivity is high fuel prices. The continued conflict in the Middle East continues to limit near-term relief, keeping fuel prices elevated. On average, fuel prices remain roughly 40% higher than pre-conflict levels, placing sustained pressure on consumer behavior and overall market momentum.

“Even after the conflict subsides, it will take an extended period of time for the price of refined products to decrease. March’s used truck market data reflects the first partial month of these high fuel prices, so the full impact may show up more clearly in April’s results,” J.D. Power adds.

For more information, and to read the entirety of this month’s report, please CLICK HERE.