The Class 8 used truck market had its best month of the year in March, with pricing jumping up nearly 22 percent in the auction channel and 4.7 percent in the retail channel, J.D. Power reported Friday in its April 2021 Commercial Truck Guidelines industry report.

The company reports auction pricing for the newest-available sleeper tractors "continues to shoot into the stratosphere." Late-model sleeper tractors are bringing the highest pricing since the company began tracking the segment in 2015 and there doesn't appear to be any reason to question March's prices. "The market has spoken," the company says.

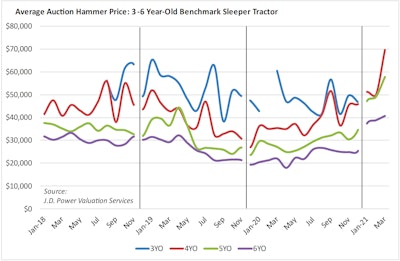

The company says auction prices in its benchmark model were as follows:

- Model year (MY) 2018: $69,556 average; $19,627 (39.3 percent) higher than February

- MY 2017: $57,749 average; $8,671 (17.7 percent) higher than February

- MY 2016: $40,639 average; $1,858 (4.8 percent) higher than February

- MY 2015: $27,192 average; $4,848 (15.1 percent) lower than February

- MY 2014: $23,570 average; $3,230 (12.1 percent) lower than February

In comparing to February, J.D. Power says its benchmark group of 4- to 6-year-old trucks brought 21.9 percent more than February. The same segment was up 72.5 percent when compared to the first quarter of 2020, which is still mostly a pre-COVID 2020 comparison, the company states.

"We don’t expect another 39.3 percent increase in any month over month results, but we do expect the newest trucks in the marketplace to remain a sure bet into the summer," the company adds.

Pricing didn't jump quite as much in the retail space but was still up — a great sign for the market considering a large corresponding increase in volume.

RELATED: Used market hits again with strong March sales

The average sleeper tractor retailed in March was 68 months old, had 458,197 miles, and brought $57,489. Compared to February, J.D. Power says this average sleeper was three months newer, had 8,774 (2.0 percent) more miles, and brought $3,102 (4.7 percent) more money. Compared to March 2020, this average sleeper was one month newer, had 3,187 (0.7 percent) more miles, and brought $13,148 (29.7 percent) more money.

J.D. Power states the lower averages for model-years 2020 and 2019 above are due mainly to a larger number of higher-mileage trucks sold, which the company's mileage adjustment probably did not adequately address in this context.

"Retail pricing is strong, but not amazing by historical standards," the company adds. "Currently, pricing is similar to early 2019. However, sales volume is higher right now, so it is accurate to say market conditions are at least as strong as the last peak."

Retail sales also leapt in March, with dealers selling an average of 5.9 trucks per rooftop. That number was 1.3 trucks higher than February and the strongest single month in J.D. Power's reporting since 2014.

"March is typically a stronger month for dealership traffic, and this year the need for late-model trucks is the most critical in at least a few years. Year over year, the first three months of 2021 are running a healthy 1.5 trucks ahead of the same period of 2020. We expect dealership traffic to remain solid through the second quarter," the company says.

Prices were up across the board in the medium-duty space as well. Class 3-4 cabovers averaged $20,074, $1,035 (5.4 percent) higher than February, and $9,436 (88.7 percent) higher than March 2020. J.D. Power notes here that March 2020’s average was unusually low, so this increase is amplified. Class 4 conventionals averaged $25,713, $2,977 (13.1 percent) higher than February, and $6,768 (35.7 percent) higher than March 2020. Finally, Class 6 conventional trucks averaged $25,709 in March, a $2,657 (8.5 percent) higher than February, and $2,572 (8.1 percent) higher than March 2020.

The company says this data should give the used truck market confidence for the second quarter, and potentially later into the year.

RELATED: As-is used truck sales offer alternative to costly reconditioning

"The newest trucks in the marketplace should see mild to moderate retail appreciation through the second quarter if not longer," J.D. Power says. "Older, higher-mileage trucks are seeing less demand. We still think a higher returning supply of trades combined with a more historically-typical freight environment could limit price appreciation somewhat in the second half of the year. However, these fundamentals could be largely negated by continued new truck constraints and extremely strong consumer spending."

Additionally, with new truck deliveries down by more than 6,000 units per month from its December 2019 high, component constraints could extend the pace at which trucking's new order boom is distributed to the market. OEMs are leaning on President Biden to assist them with this challenge, but to this point those requests have not netted them any supply chain enhancements.

And J.D. Power also notes dealers should "keep in mind the repair and replacement parts business is impacted as well, adding incremental demand for used trucks.

"In view of all this, our prediction that late-model trucks will remain a solid bet into the summer is pretty much a lock, and we won’t be surprised if this dynamic is in place well into the second half of the year. We’ll stop short of guaranteeing a hot market for all of 2021, but March’s results add optimism to our assumptions."

For more information, and to read the entirety of this month’s report, please CLICK HERE.