Even with a stronger than anticipated March, ACT Research states three months into 2026 and the U.S. trailer industry remains mired in the same challenging environment in which it operated throughout 2025.

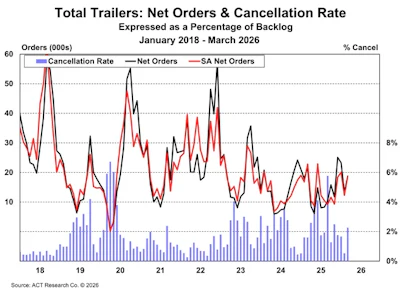

“Demand for trailers improved in March, but demand was weak across Q1,” says Jennifer McNealy, director of commercial vehicle market research and publications at ACT Research. “Carrier profits, although benefitting from an uptick in freight rates and a tightening driver pool, remain low, with government policy and geopolitical instabilities keeping customers cautious. With equipment demand fundamentals transitioning in Q1, net order intake in March jumped to 18,800 units, up more than 42% from February. This brought the first quarter 2026 order tally to 55,400 trailers, about 9% less than were ordered during the first quarter 2025.”

McNealy does note cancellation rates have improved, finding a “more subdued” pace to start the year. “March’s rate of 2.3%, as a percentage of backlog, returned the industry cancellations to ‘elevated’ territory from the middle of the acceptable range reported last month. Unlike the last few months, though, data in March showed high cancellations in nearly all segments,” McNealy says.

[RELATED: PacLease’s Roemer to chair TRALA for upcoming year]

Finally, after a one-month hiccup in February, net orders again outpaced build in March, but she says this time it wasn’t by enough to pump much lifeblood into the anemic backlogs.

“Backlogs grew 3% sequentially, or about 2,200 units, bringing the Q1-ending BL to 76,400 units, or 23% lower than the Q1 25-ending, 99,300-unit trailer backlog. The backlog-to-build ratio was 4.7 months at the end of 2026’s first quarter,” she says.