January was an expectedly slow month for used truck auction activity and the lack of movement was clear in sales data, J.D Power reported Friday in its February Commercial Truck Guidelines report. In the retail space, sleeper pricing outpaced January 2024 but daycabs had a tougher month.

“With very few auctions on the calendar in the first half of the month, January is typically the slowest month of the year. January 2025 was no exception,” the company says. “This low volume of sales combined with a very wide range in mileage skewed the averages in our table lower than actual market movement.”

That said, looking at late-model sleeper tractors, J.D. Power states average pricing for our benchmark truck in January was:

- Model year (MY) 2023: $83,651; $2,599 (3.0%) lower than December

- MY 2022: $58,389; $7,924 (11.9%) lower than December

- MY 2021: $41,005; $5,993 (12.8%) lower than December

- MY 2020: $39,772; $1,619 (3.9%) lower than December

- MY 2019: $24,512; $2,738 (10.0%) lower than December

The company adds that as of this month, it is now considering “4-to-6-year-old” to include model years 2022-2020. With that in mind, selling prices for that group in January 2025 were nearly identical to January 2024, with less than 1% separating the two periods. Pricing for that cohort is currently 16.6% higher than the strong pre-pandemic period of 2018 in nominal figures (7.0% lower if adjusted for inflation), and 75.3% higher than the last market nadir in late 2019 (42.7% higher if adjusted for inflation). Month-over-month comparisons will return next month, J.D. Power notes.

[RELATED: J.D. Power tackles used market dynamics, sees reason for optimism]

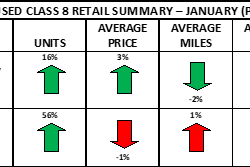

In the retail market, sleeper pricing was stronger year over year. Daycabs did not show the same strength.

Overall, J.D. Power states the average sleeper tractor retailed in January was 62 months old, had 439,715 miles and brought $61,365.

Compared with December, this average sleeper was one month older, had 44,024 (11.1%) more miles and brought $4,355 (7.6%) more money. Compared with January 2024, this average sleeper was nine months newer, had 3,381 (0.9%) fewer miles and brought $897 (1.4%) less money.

The company adds January’s average pricing for late-model trucks was as follows:

- MY 2024: $140,415; $20,726 (17.3%) higher than December

- MY 2023: $95,124; $18,270 (16.1%) lower than December

- MY 2022: $78,284; $13,603 (21.0%) higher than December

- MY 2021: $55,996; $3,711 (6.2%) lower than December

- MY 2020: $52,901; $9,821 (22.8%) higher than December

- MY 2019: $34,743; $3,837 (9.9%) lower than December

In the 3-to 5-year-old cohort, sleeper tractors brought 14.4% more than January 2024. Late-model sleepers are now bringing 38.6% more money than the last strong pre-pandemic period of early 2019 in nominal dollars, or 10.3% more when adjusted for inflation. Compared with the last weak pre-pandemic period, late-model sleeper values are running 58.9% higher in nominal dollars or 28.5% lower in real dollars.

J.D. Power says month-over-month and depreciation averages will return next month.

Moving to the daycab segment, the company states trucks sold retail in January brought 4.8% less money than January 2024. J.D Power adds it will have “more analysis of this segment next month, after more auction data is in the books.”

Finally on the topic of volume, dealers sold 2.6 trucks per rooftop in January, 0.4 truck less than a strong December 2024, but 0.2 truck higher than January 2024. The total number of retail sales reported in January was 22.8% lower than December 2024, but 6.1% higher than January 2024.

“Negative equity and access to credit will remain a challenge to retail buyers, but the freight environment is still generally improving, which could support retail activity in upcoming months,” the company notes.

For more information, and to read the entirety of this month’s report, please CLICK HERE.