Sales volumes at auctions and on dealer lots hit seasonal lows in February, J.D. Power reported Thursday in its March Commercial Truck Guidelines report, and auction prices are down.

Historically, February is the second-lowest month of the year in terms of sales volume, and the month met expectations. Pricing showed some mild depreciation compared to January. Pricing for the benchmark late-model sleeper truck in February was:

- Model year (MY) 2023: $81,700, 2.3% or $1,951 lower than January.

- MY 2022: $58,088, 0.5% or $301 lower than January.

- MY 2021: $38,340, 6.5% or $2,665 lower than January.

- MY 2020: $37,131, 6.6% or $2,641 lower than January.

- MY 2019: $24,672, 0.7% or $160 higher than January.

Selling prices at auction for benchmark trucks four to six years old averaged 4% less than in January, but 8.9% higher than in February 2024. Pricing for the group is 11.9% higher than the pre-pandemic period in 2018 in nominal figures (2.5% lower if adjusted for inflation), and 79.1% higher than the last market dip in late 2019 (44.2% higher if adjusted for inflation). Trucks four and five years of age dropped for a second consecutive month. Year-over-year pricing comparison remains positive, as it has been since November 2024, the company says.

[RELATED: Doing the math on a prospective used truck sale]

Daycab values continue to slip, J.D. Power says, while sleeper pricing stayed stable. The average sleeper tractor sold in February was 64 months old, had 436,135 miles and sold for $62,791. That's two months older than in January, with 3,580 fewer miles and $1,426 more expensive. Compared with February 2024, the average sleeper was seven months newer, with 327 more miles and $391 more expensive.

February's average pricing for late-model trucks was:

- Model year 2024: $141,460, 0.7% or $1.045 higher than January.

- Model year 2023: $78,066, 0.3% or $218 lower than January.

- Model year 2021: $55,987, flat from January.

- Model year 2020: $47,321, 10.5% or $5,580 lower than January.

- Model year 2019: $31,993, 7.9% or $2,750 lower than January.

Sleeper tractors three to five years old brought slightly (0.2%) more than January and 3.8% more than February 2024. Late-model sleepers are bringing 22.7% more money than in the strong pre-pandemic in nominal dollars or 2.8% less when adjusted for inflation. Compared with the weak pre-pandemic period, late-model sleepers are 59.1% more expensive in nominal dollars or 28.2% in real dollars. There was no depreciation from January to February.

Daycab trucks in February were 14.4% less expensive than January and 12.8% less expensive year-over-year. Daycabs continue to underperform sleepers and supply is still oversaturated.

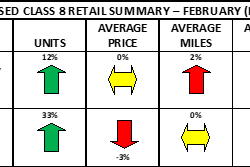

Dealers sold just 1.9 trucks per rooftop, slower than January and slower than February 2024. Total retail sales in February was 13% lower than January and 15.8% lower than February 2024.

J.D. Power says negative equity will remain a challenge this year, but pricing "continues to trend horizontal." An expected surge in trades later this year from a 2027 pre-buy may be more muted thanks to possible changes in regulations, as well as unpredictable freight dynamics from tariffs and trade policies.

For more information, and to read the entirety of this month’s report, please CLICK HERE.