Volume decreased in the auction lanes in July 2025, but dealers sold more trucks off their lots. J.D. Power announced last week in its August Commercial Truck Guidelines report. Pricing also declined in both channels in July.

J.D. Power states July is typically a slow month for Class 8 auctions, and this year was no exception. Volume declined from June and there was no notable pricing movement in the sleeper tractor segment in general.

Looking at late-model sleeper tractors, the company says average auction pricing for its benchmark truck In July was:

- Model year (MY) 2023: $83,325; $18,333 (28.2%) higher than June

- MY 2022: $45,369; $8,590 (15.9%) lower than June

- MY 2021: $42,203; $6,699 (18.9%) higher than June

- MY 2020: $34,727; $3,207 (10.2%) higher than June

- MY 2019: $24,126; $1,538 (6.8%) higher than June

[RELATED: ACT reports low trade activity in July used truck market]

At auctions in July, selling prices for the 4- to 6-year-old cohort of benchmark truck averaged 1.1% higher than June, and 0.6% lower than July 2024. Pricing for that group is currently 7.4% higher than the strong pre-pandemic period of 2018 in nominal figures (16.1% lower if adjusted for inflation), and 64.0% higher than the last market nadir in late 2019 (30.7% higher when adjusted for inflation), J.D. Power says.

Additionally, the company adds deprecation for this group has accelerated mildly in 2025, now averaging 1.8% per month.

“As usual, the limited volume of trucks sold each month results in swings in the raw data averages that are not necessarily reflective of actual market movement,” J.D. Power reports.

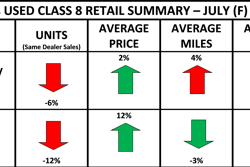

In the retail space, price slipped for the first time since December 2024 but volume was up notably from June.

Looking at the overall mix of trucks retailed in July, J.D. Power states dataset of sold sleeper tractors averaged 54 months old and 429,797 miles. Compared with June, this group was two months newer and had 9,443 (2.2%) fewer miles. Compared with July 2024, this dataset averaged 10 months newer and 9,985 (2.3%) fewer miles. J.D. Power says retail customers continue to become more selective in terms of age and mileage of trucks they’re willing to accept.

[RELATED: It’s hard to find good news in an economic forecast these days]

Overall, July’s average pricing for late-model trucks was as follows:

- MY 2024: $121,226; $9,481 (7.3%) lower than June

- MY 2023: $100,416; $2,362 (2.3%) lower than June

- MY 2022: $77,053; $759 (1.0%) lower than June

- MY 2021: $60,828; $1,078 (1.8%) higher than June

- MY 2020: $46,036; $2,096 (4.7%) higher than June

J.D. Power states 3- to 5-year-old sleeper tractors brought 3.1% less than June and 25.3% more than July 2024.

“Year-over-year comparisons have been positive since December 2024, but July was the first month of 2025 to see a month-over-month decrease,” the company says. “Late-model sleepers are now bringing 19.1% more money than the last strong pre-pandemic period of early 2019 in nominal dollars, or 7.2% less when adjusted for inflation.

“Compared with the last weak pre-pandemic period of late 2019, late-model sleeper values are running 54.5% higher in nominal dollars or 22.9% higher in real dollars. Despite July’s month-over-month dip, depreciation in 2025 to date is still averaging well under 1% per month.”

On a dealership perspective, J.D. Power reports retail sales per dealership increased notably to an average of 3.4 trucks sold in the month. There have now been three months in 2025 with sales above 3.0, compared to none in 2024. The total number of retail sales reported in July was 11.3% lower than June, and 0.5% higher than July 2024.

In looking ahead, J.D. Power assessment is mostly muted.

“EPA 2027 regulations are all but rolled back at this point, providing some motivation for new truck buyers to plan their purchases over the next 18 months. However, prices will still increase due to tariff-induced materials costs and the R&D that was already done on EPA 2027 drivetrains.

“The freight market remains depressed and used truck conditions won’t change much until more trucks are removed from the nation’s fleet with a concurrent increase in manufacturing and consumer spending.”

For more information, and to read the entirety of this month’s report, please CLICK HERE.