This year is unlikely to a be record setter for medium- and heavy-duty truck sales.

Speaking Tuesday during a market overview and update session at Work Truck Week in Indianapolis, NTEA’s Steve Latin-Kasper and Andrej Divis with S&P Global Mobility reported their businesses are predicting very little change for the Class 4 to 8 markets in 2023.

Though Latin-Kasper was careful to avoid the ‘R’ word, Divis said S&P’s base predictions for equipment sales in 2023 presume a very mild economic recession during the year. The duo say the recession, if it occurs, is unlikely to be deep or long-lasting, but in any event it will likely lead to muted sales growth when evaluating 2023 on a year over year scale.

Coming off a 2021 and 2022 where sales demand occasionally far exceeded production capacity, the economists say 2023 will likely see the Class 4 to 8 market segments continuing their regression to pre-pandemic cycle norms. A slowly improving supply chain will help bring reduce backlog totals across the medium- and heavy-duty sectors, while an infusion in spending due to the bipartisan infrastructure package and Inflation Reduction Act should stimulate purchasing in some segments to counteract any sales softening in others (such as housing and e-commerce).

[RELATED: Inflation becomes top concern for trucking suppliers]

“Should we see a recession, it will probably be in the second half of the year,” says Latin-Kasper. “It is unlikely to cause a significant number of problems for your businesses going forward.”

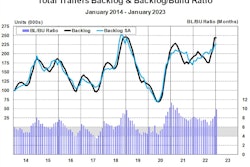

He says where Work Truck Week attendees are likely to see feel pressure this year is the same places they were pinched in 2022. Latin-Kasper says it is unlikely the Federal Reserve will be able to reduce inflation down to its target, meaning interest rates will remain higher than ideal throughout the year. The supply chain also will continue to be frustratingly stressed. Latin-Kasper says there “tens of thousands of chassis still parked” waiting to be completed and says those units will remain a challenge for OEMs throughout the year.

“I think we still have a situation where from one OEM to another, supply chain disruptions are still affecting them all a little bit differently,” he said. “We probably won’t get to a normal inventory situation until 2024.”

Divis says S&P’s 2023 forecast is a slight decrease in Class 8 sales with a small uptick in the Class 4-7 markets. The company’s 2024 forecast is even softer with a strong market correction expected in 2025.

[RELATED: Truck order reverse trend, rise slightly in February]

On a class-by-class basis, Divis says the Class and 4 and 6 segments are expected to be strong with the Class 5 market bottoming out then recovering after its immediate post-COVID 2021 sales boom. He says the Class 7 market has been underproduced for nearly a decade and will grow if production capacity allows. Class 8 demand will be steady; large carriers finally began turning over their oldest units last year and will continue doing so with orders placed in 2023 and 2024.

Questioned on allocation, both economists were hesitant to speak for the OEMs but noted it is unlikely any manufacturers are able to take the restrictor plate off their production lines in 2023 — nor would they likely want to. Demand is not extraordinarily high as it was in 2021; carriers have orders submitted and have adapted longer delivery times.

“I don’t think we’re in a position yet where OEMs can build everything customers have asked for,” says Divis. “With the backlogs and [the supply chain] lead times. I don’t see potential to raise the line rates much.”