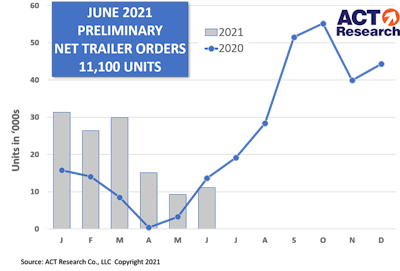

Preliminary reports show trailer OEMs posted 11,100 net orders in June, 20 percent above May orders, but 19 percent below the same point last year, according to ACT Research’s State of the Industry: U.S. Trailers report.

Meanwhile, FTR reports continued softness in preliminary trailer orders in June, coming in at 11,000 units, 16 percent above a weak May and down 24 percent year over year. Trailer orders for the past 12 months total 364,000 units.

“While the sequential increase in net orders was certainly welcome, a full response to actual fleet demand would have generated higher order volumes. Some OEMs, due to their extended backlogs, continue to be unwilling to book meaningful order volumes at this time,” says Frank Maly, director, CV Transportation Analysis and Research at ACT.

“June’s negative year-over-year comparison for net orders was the first since May 2020, the tail-end of last spring’s COVID-depressed order activity. These preliminary results point to a backlog that still extends into late Q1 of next year on average, with dry van and reefer backlogs extending into Q2 of 2022 at current production rates,” Maly says.

“While total production did improve last month, the gains came from additional days in the production schedule. Preliminary analysis indicates OEMs were not able to achieve any significant increase in build rates during the month, as headwinds from material and component supplies, as well as staffing challenges, continue,” he says.

FTR reports order activity was constrained, as most OEMs are not taking additional orders for 2021 delivery. However, vocational trailer orders were steady, as there are still open build slots in those segments. The industrial sectors of the economy recovered slower than the consumer side, delaying the demand for flatbeds and tank trailers.

“The market is in a holding pattern until ordering for 2022 shipments begins. Demand for trailers remains robust, as fleets attempt to move an increasing amount of freight during a shortage of Class 8 trucks. Fleet capacity is extremely tight. Trailer production is also constrained by supply chain disruptions and labor shortages,” says Don Ake, FTR vice president of commercial vehicles.

“Orders are expected to set records once the order boards for 2022 are opened. Trailer demand is expected to be sturdy throughout next year. However, the actual demand for trailers will not be ascertainable until the supply chain problems dissipate,” Ake says. “The production situation for early 2022 could be complicated if OEMs cannot build all the orders currently on the books in 2021.”