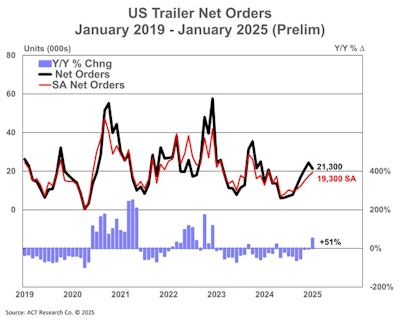

January trailer orders were down slightly from December 2024 as demand continues to slip against last year's strong seasonal showing, FTR and ACT Research reported Tuesday. FTR estimates last month's orders at 23,966 units, down 2% from December. ACT pegs January even lower at 21,300 units.

The two firms state January's orders are well ahead of January 2024 but, overall, the market is not as strong as it was a year ago. FTR reports during the season ordering season of September to January, current orders are 98,926 units — 19,785 per month — down 21% from the same period a year ago.

ACT adds seasonal adjustment at this point in the annual order cycle even further lowers January’s tally to 19,300 units, still above December but down against historical data.

“Many fleets continue to prioritize purchasing power units over trailers — a trend unlikely to reverse given the approaching implementation of EPA’s 2027 NOx regulations on trucks,” says FTR's Dan Moyer, senior analyst, commercial vehicles. “During the 2025 order season so far, North American Class 8 net orders are up 4% year over year while U.S. trailer net orders are down 21%. Trailer OEMs have scaled back production, and prolonged cuts are possible if demand remains weak.”

[RELATED: State of Georgia recognizing Great Dane for 125-year anniversary]

Adds Jennifer McNealy, ACT's director of commercial vehicle market research and publications, “Though past the traditional peak, we’re still in a period of ‘strong order’ intake. This month’s pattern of lower than December but still above average demand was expected. It’s also no surprise that the data are higher than the January 2024 intake, given the slowing demand that marked 2023 and led into the subdued market reported throughout most of 2024.”

McNealy also notes “Notwithstanding the improvement thus far in the 2025 order cycle, ACT’s expectations for weak trailer demand relative to recent performance remain, as continuing weak for-hire truck market fundamentals, low used equipment valuations, relatively full dealer inventories and high interest rates impede stronger activity in the near term. An order uptick showcasing demand, or the lack thereof, depends not just on the first few months of the new order cycle, but on order volumes through [the first quarter of] 2025 and beyond.”

On the topic of production, FTR reports January builds were up 2% month over month but down 35% year over year and 46% below the seven-year January average. January was the second lowest monthly output since 2010, only outpacing December. The company says backlogs increased by 12,210 units, pushing the backlog/build ratio up to 9.7 months — the highest since February 2023.

While this higher ratio is largely attributed to exceptionally low production levels, it also suggests easing pressure on OEMs to further scale back production in the near term, FTR states.

“Tariffs threaten further disruption,” adds Moyer. “The 25% tariffs on steel and aluminum imports planned to take effect next month along with the 10% additional tariff already imposed on Chinese imports and the currently paused but still possible 25% tariffs on Canadian and Mexican imports will raise material costs, squeeze margins, and strain supply chains. Tariffs will affect not only fully assembled trailers imported into the U.S. but also domestically produced trailers, which depend on imported materials and components.

“Expect market volatility as OEMs try to adapt to uncertainty over scope and timing of tariff impacts.”