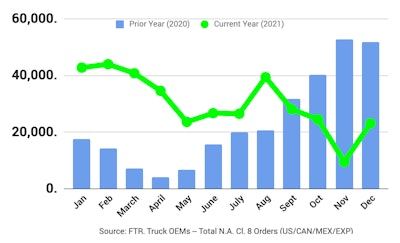

Preliminary Class 8 net orders in December were 22,800 units, while Class 5-7 net orders dropped to 18,100 units, a significant sequential uptick for Class 8 but lower month-over-month and year-over-year readings for the medium-duty market, according to ACT Research’s State of the Industry: Classes 5-8 Vehicles report. FTR reports Class 8 net orders recovered to 23,100 units in December and totaled 365,000 units for the year.

“For Class 8, with backlogs stretching through 2022 and still no clear visibility on the easing of the ‘everything shortage,’ modest December net orders reflect OEMs taking a more cautious approach to effectively manage the cycle of customer expectations,” says ACT President and Senior Analyst Kenny Vieth.

“With a 12-month BL/BU ratio and the industry only reporting units scheduled to be built within 12 months, some of the current order constraint is built into the data collection process: If the BL/BU is 12 months, new orders are ultimately consigned to the level of industry production,” Vieth explains.

“After hitting a [Class 8] cancellation speed-bump in November, orders rebounded to a level just above the second half of 2021 production trend in December. However, while improved, December’s orders were the second weakest of the year, reflecting ongoing supply-side shortages that continue to constrain production. Importantly, we reiterate, with critical economic and industry demand drivers at, or near, record levels, industry strength is exhibited in long backlog lead-times, rather than in seasonally weak orders,” Vieth says.

FTR reports the December total orders for Class 8 trucks were back in the same range as September and October, following the previous trend of orders being slightly above expected production levels. December order activity was up 139 percent month over month, but still down 55 percent year over year from December 2021.

The December number is positive in the sense that all OEMs entered some orders. This indicates at least some optimism about improved future supply chain performance. OEMs are content in keeping backlogs at current levels and continue to enter orders a portion at a time due to uncertain supply chain conditions, according to FTR.

“The current order volume still understates the tremendous demand for new trucks. The OEMs have a large number of fleet commitments for 2022. They are delaying entering these orders until they know how many they will be able to build each month. Supply chain delays continue to constrain build rates,” says Don Ake, FTR vice president of commercial vehicles.

“Fleets need a considerable number of new trucks right now. Industry capacity is extremely tight, resulting in elevated freight rates. The carriers have freight to haul and funds available for new trucks, but OEMs can’t build enough. Also, the large fleets have had to run vehicles beyond their trade-in cycles and need replacement trucks,” Ake says.