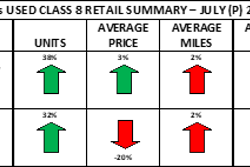

Volumes in the auction market were down last month while pricing in the auction and retail segments showed little change, J.D. Power reported Thursday in its August 2024 Commercial Truck Guidelines report.

In the auction space, volumes were down significantly from June, which the company says is typical for the month. Selling prices increased notably, although J.D. Power says the small sample size means the company is not drawing any conclusions from this month’s results just yet.

Looking at late-model sleeper tractors, J.D. Power says average pricing for its benchmark truck in July was:

- Model year (MY) 2021: $49,075; $5,406 (12.4%) higher than June

- MY 2020: $40,065; $2,103 (5.5%) higher than June

- MY 2019: $33,911; $7,333 (27.6%) higher than June

- MY 2018: $22,173; $5,418 (32.3%) higher than June

In July, the company says selling prices for 4- to 6-year-old sleepers were 13.7% higher than June. July’s upward bump brought pricing back into parity with the strong pre-pandemic period of 2018 in nominal figures, or about 21% lower if adjusted for inflation. Additionally, the company reports current pricing is now about 55% higher than the last market nadir in late 2019, or about 27% higher if adjusted for inflation.

[RELATED: Register now for our upcoming webinar on bolstering your bottom line!]

And depreciation in 2024 is now averaging 1.9% per month, lower than the historical average.

"One thing we can say for certain about July’s results is trucks didn’t lose value compared with June. In that respect, the figures represent more evidence of a price floor, at least in the auction lanes," the company says.

In the retail space, volume recovered June’s dip and pricing was incrementally lower. Overall, J.D. Power says the average sleeper tractor retailed in July was 64 months old, had 439,782 miles and brought $61,632. Compared with June, this average sleeper was four months newer, had 8,992 (2.0%) fewer miles and brought $5,185 (9.2%) more money. Compared with July 2023, this average sleeper was ten months newer, had 24,779 (5.3%) fewer miles and brought $5,008 (7.5%) less money, the company says.

July’s average pricing for late-model trucks was as follows:

- MY 2023: $110,092 $10,861 (9.0%) lower than June

- MY 2022: $91,377; $2,665 (2.8%) lower than June

- MY 2021: $69,828; $2,731 (3.8%) lower than June

- MY 2020: $50,627; $3,313 (6.1%) higher than June

- MY 2019: $41,856; $1,359 (3.2%) higher than June

- MY2018: $29,078; $312 (1.1%) higher than June

J.D. Power adds 3- to 5-year-old sleeper tractors brought 1.0% less money in July than June, and 8.3% less than July 2023. The company reports late-model sleepers are bringing slightly less money than the last strong pre-pandemic period of early 2019 in nominal dollars, or 21% less when adjusted for inflation.

Compared with the last weak pre-pandemic period, late-model sleeper values are running 22% higher in nominal dollars or essentially equal money in real dollars. Depreciation in 2024 is averaging 2.3% per month, which is historically typical, the company says.

Moving to the daycab segment, J.D. Power says a comparatively low volume of retail sales reported makes it difficult to clearly identify month-over-month market movement, but a review of auction data supports the assessment this segment is in a correction.

[RELATED: UTA Convention early bird registration available]

In July, late-model daycabs brought 11.8% less money than June (retail). Compared with July 2023, this segment brought 32.6% less money. Average monthly depreciation in 2024 for this segment is now substantially higher than historical trend as well as the sleeper segment, at 4.1%. Heavier-spec tractors and those with low mileage are still bringing strong money, but typical highway-spec, 13L units with average mileage have depreciated heavily in the third quarter, the company says.

Fortunately, volume was up. J.D. Power reports dealers sold 2.5 trucks per rooftop in July, 0.8 higher than June, and equal to May. Overall, 33% more trucks were reported sold retail in July vs. June. The CDK Global hack/outage was partly responsible for June’s low volume and caused many sales to be recorded in July. As such, we expected July’s results to be slightly higher than they were, the company says.

For more information, and to read the entirety of this month’s report, please CLICK HERE.