If there’s been a silver lining to this year’s weak freight environment, it’s been the stability of inventory in the used truck space.

This was supposed to be the year of freight’s bounce back. The year of the pre-buy and its cascading flurry of big trade packages. Instead it’s been the year of tariffs, of economic uncertainty and reduced capital expenditure.

Replacement demand has been the driver of purchases across the spectrum, and while that’s unquestionably limited demand, it’s also kept used truck volumes reasonably steady. It’s created a marketplace where the best trucks are snatched up quickly, and at a premium, but less-enticing units must be moved tactically to be profitable.

And barring any sudden freight shift, experts think that’s likely to continue as the year concludes.

“Had there been a pre-buy, it would have created a pull ahead in new truck and trade-in activity and an oversupply of used trucks, and the last thing the [used truck] industry needs now is more trades,” says Chris Visser, director of specialty markets at J.D. Power.

But if they aren’t coming, Visser says the market is positioned to manage replacement demand.

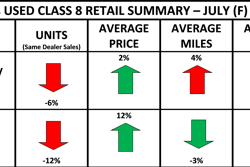

He says late-model, low-mileage trucks have been in high demand in the retail sector all year and the overall increase in price (seen in the Price Digests by Fusable chart below) and minimal depreciation they’ve experienced bears that out. And without a pre-buy, used dealers don’t need to worry about a large influx of those units hitting the market and overwhelming supply.

In fact, if freight could improve at all, the market could have “some perception of scarcity,” says ACT Research Vice President Steve Tam. As it is, Tam says used dealers who are not over reliant on for-hire carrier buyers — “those guys have had their teeth kicked in all year” — can still swiftly move good equipment.

[RELATED: Register now for the 2025 UTA Convention]

Tam advises dealers look for small private fleets, owner-operators and carriers with “viable business models” who have been able to shield their operations from the worst of the 2025 freight marketplace to move their day cab and sleeper equipment. He doesn’t advise targeting regional hot spots, however, which have been unpredictable.

“Our regional heat map has kind of been a moving target,” he says. “Take Indiana as an example. One month it will be green and then it turns red. There are no areas that are consistently good.”

Tam and Visser also believe President Donald J. Trump’s new tariffs on steel and aluminum derivatives will increase new truck production costs, but not enough to drive a large subset of carriers into used truck purchases. Nor will any regulatory rollbacks.

“I don’t want to dismiss the tariffs, but the traditional buyers who order new equipment are not suddenly going to consider used trucks because of the tariffs,” says Tam. “If the tariffs amount to $10,000 on a $170,000 unit, if you’re on a fixed cap-ex budget, maybe that reduces the total number of trucks you can buy, but you still place your order.”

Visser agrees. “Last time manufacturing was impacted by tariffs was 2019 and one analysis at the time indicated manufacturers absorbed 60% of the tariffs, on average.” He admits it’s unlikely OEMs will absorb that much additional expense in this climate — the tariffs are much more severe — but still finds it unlikely large carriers with fixed budgets will suddenly pivot into pre-owned purchasers.

“I’ve only heard one customer who said they would flat out refuse to pay the tariffs,” adds Tam. “And not because of the price, but out of principle.”

Additionally, Visser notes a possible amendment or delay of the EPA’s NOx rule would lower expected new technology costs and make it easier for tariff increases to be absorbed by new truck purchasers.

“I think [higher prices] will be within the boundaries of what would be considered normal,” he says.

[RELATED: Truck orders continue year-over-year descent]

Stepping out of the retail space, the duo sees muted positivity in the auction and wholesale markets as well.

Visser points to the aforementioned absence of trade packages, which should keep inventory and pricing steady. Tam notes there’s also a healthy portion of owner-operator shoppers on the auction circuit, looking for value in older, low-priced equipment. Those customers are on a budget but pay with cash, and give dealers an option when equipment needs to be moved.

After seven years of above-average replacement demand in the new truck space, Tam says used truck dealers are fortunate inventory levels aren’t higher (like their new truck counterparts). And if carriers continue to delay new truck purchases, the used market should remain shielded from supply-side volatility that would disorient pricing.

But soft freight metrics also put limitations on used truck demand, and a robust albeit unpredictable market offers more sales potential than a controlled environment.

“We need the economy to come to the party,” says Tam.